Dividend Growth Investing & Retirement is supported by its readers through donations and affiliate links. If you purchase through a link on my site, I may earn a commission. Thanks! Learn more.

Wide moat companies are a natural starting point for investors looking for high-quality stocks.

To help with this search, I used Morningstar to find all Canadian wide moat stocks.

⭐ Find dividend growth stocks that have survived multiple recessions and increased dividends for 5, 10, 25+ years in a row.

Results below …

Canadian Wide Moat Stocks from Morningstar Analyst Ratings

Drum roll, please…

Only 6 companies in all of Canada?

I was surprised too.

I’ll get to some of the surprises (Telecoms, Utilities and a few others) that didn’t make the list later on in the article.

For now, here’s the list:

As of September 2020

- Canadian National Railway Co (TSE:CNR; NYSE:CNI)

- Canadian Pacific Railway Ltd (TSE:CP; NYSE:CP)

- Enbridge Inc (TSE:ENB; NYSE:ENB)

- Royal Bank of Canada (TSE:RY; NYSE:RY)

- The Toronto-Dominion Bank (TSE:TD; NYSE:TD)

- Waste Connections Inc (TSE:WCN; NYSE:WCN)

And there you have it, every wide moat stock in Canada.

But not so fast …

There are an additional 3 stocks that have a wide moat quantitative rating vs. a wide moat rating made by a real person (an analyst), like the 6 stocks above.

Before I share these last 3 stocks, I have a few words of caution. Well, maybe more than a few …

265 Words Of Caution on Wide Moat Quantitative Ratings

When trying to determine if a company has a wide moat, a quantitative rating is less reliable than a rating made by an analyst.

For stocks that aren’t covered by Morningstar analysts they give a quantitative rating – basically a computer formula figures it out instead of a person.

Or as Morningstar puts it:

“Morningstar Quantitative ratings for equities are generated using an algorithm that compares companies that are not under analyst coverage to peer companies that do receive analyst-driven ratings. Companies with ratings are not formally covered by a Morningstar analyst, but are statistically matched to analyst-rated companies, allowing our models to calculate a quantitative moat, fair value, and uncertainty rating.”

Quantitative ratings are good for some things, but understanding a company’s competitive advantages and how sustainable they are, isn’t necessarily one of them.

Warren Buffett said in the 1999 Berkshire Hathaway annual meeting that (emphasis added):

“No formula in finance tells you that the moat is 28 feet wide and 16 feet deep. That’s what drives the academics crazy. They can compute standard deviations and betas, but they can’t understand moats. Maybe I’m being too hard on the academics.”

I think this comment still holds true and who am I to argue with one of the greatest investors of all-time.

If Warren Buffett thinks understanding a moat is difficult for academics used to creating a formula for everything, then I don’t think quantitative moat ratings are going to be as reliable as the analyst ones.

Bottom line: I put more weight in the Morningstar moat ratings that are made by analysts compared to the quantitative ratings.

Canadian Wide Moat Stocks From Morningstar Quantitative Ratings

OK, now that I’ve got my warning out of the way, here are the remaining 3 wide moat stocks using Morningstar’s quantitative ratings.

As of September 2020

- Constellation Software Inc (TSE:CSU)

- Enghouse Systems Ltd (TSE:ENGH)

- Franco-Nevada Corp (TSE:FNV; NYSE:FNV)

Some Surprises That Didn’t Make The List (Telecoms, Utilities And A Few Others)

If you were surprised that a company didn’t make it on to the wide moat list, it’s likely because Morningstar has it rated as narrow-moat instead of wide.

So, what’s the difference between a wide and narrow moat?

The wide, narrow and no-moat ratings reflect how sustainable a competitive advantage is. In other words, how long will this competitive advantage last?

Wide moat = +20 years

Narrow moat = 10-19 years

No moat = 0-9 years

Now that you know the main difference between these ratings, let’s look at my first surprise, the Canadian telecoms.

Telecoms

The Canadian telecommunication market is dominated by just a few companies: For example, in wireless, BCE Inc. aka Bell (TSE:BCE; NYSE:BCE), Telus (TSE:T; NYSE:TU), and Rogers (TSE:RCI.B; NYSE:RCI) make up about 90% of the market. It’s natural to wonder why at least one of these companies wouldn’t be considered a wide moat stock.

Instead, Morningstar has all three rated as narrow-moat stocks.

A look at BCE’s May 14, 2020 Economic Moat analyst report explains why (emphasis added):

“The biggest factor keeping us from labeling BCE a wide-moat company is the ever-present threat of regulation in the telecom industry. […] the government seemingly favors more robust competition for the top three providers, as evidenced by it historically giving other competitors favored status in spectrum auctions. […] our level of confidence in long-term projections is tempered by the industry’s sensitivity to government influence.”

Government regulation for the public good is not so good for a company’s bottom line. With the threat of things like price caps, mandatory network sharing, or other competition enhancing measures a narrow-moat rating was given to the big telecom companies in Canada instead of wide moats.

Utilities

Most utility companies are considered narrow-moat stocks. The narrow-moat comes from regulated operations in service territory monopolies and efficient scale advantages.

Like telecoms, it’s regulation for the public good that typically prevents them from reaching a wide moat rating, but at the same time these regulations also help maintain a narrow-moat.

Here’s an excerpt from Morningstar’s July 30, 2020 report on the narrow moat Fortis Inc (TSE:FTS; NYSE:FTS) that explains it well (emphasis added):

“For the regulated gas and electric operations, service territory monopolies and efficient scale advantages are the primary sources of an economic moat. Regulators typically grant regulated utilities exclusive rights to charge customers rates that allow the utilities to earn a fair return on and return of the capital they invest to build, operate, and maintain their distribution networks. In exchange for regulated utilities’ service territory monopolies, regulators set returns at levels that aim to minimize customer costs while offering fair returns for capital providers.

This implicit contract between regulators and capital providers should, on balance, allow regulated utilities to achieve at least their costs of capital, though observable returns might vary in the short run based on demand trends, investment cycles, operating costs, and access to financing. Intuitively, utilities should have an economic moat based on efficient scale, but in some cases regulation offsets this advantage, preventing excess returns on capital. The risk of adverse regulatory decisions precludes regulated utilities from earning wide economic moat ratings. However, the threat of material value destruction is low, and normalized returns exceed costs of capital in most cases, leaving us comfortable assigning narrow moats to many regulated utilities.”

Other Canadian utility stocks like Canadian Utilities Ltd (TSE:CU), and Emera Inc (TSE:EMA), also have narrow moats.

The Other Big Banks

Canada is known for its “Big 6” banks, but only the two largest (Royal Bank and TD) were rated as wide moat, what about the other four?

Bank of Nova Scotia (TSE:BNS; NYSE:BNS), Bank of Montreal (TSE:BMO; NYSE:BMO), CIBC (TSE:CM; NYSE:CM), and National Bank of Canada (TSE:NA) all have narrow-moat ratings.

TC Energy Corp (TSE:TRP; NYSE:TRP) formerly TransCanada

You may be thinking, if Enbridge, a large pipeline stock, got a wide moat rating, why didn’t the other large pipeline, TC Energy, too?

It comes down to contract length. TC Energy is able to secure long contracts of over 10 years, but it’s still less than Enbridge. Enbridge is able to negotiate 20-25 year contracts on some of its regional pipelines.

Here’s what Morningstar had to say about TC Energy in their July 31, 2020 report:

“While the contracts are solid and lock in attractive economics for more than 10 years, they are not best in class. We would like to see the average remaining terms on the existing assets exceed 20 years, which is why we conclude that TC Energy has a narrow moat.”

Compare this to comments from Enbridge’s April 16, 2020 Morningstar report below, and you’ll understand why there is a difference between Enbridge’s wide moat rating and TC Energy’s narrow moat rating.

“Difficulty obtaining regulatory approval on major pipeline expansions, attractive regulated tolls that exceed the company’s cost of capital, and 20- to 25-year contracts on regional pipelines afford the company a wide economic moat.”

3 Additional Resources

Besides the other articles in my wide moat series, here are three additional resources you might find helpful.

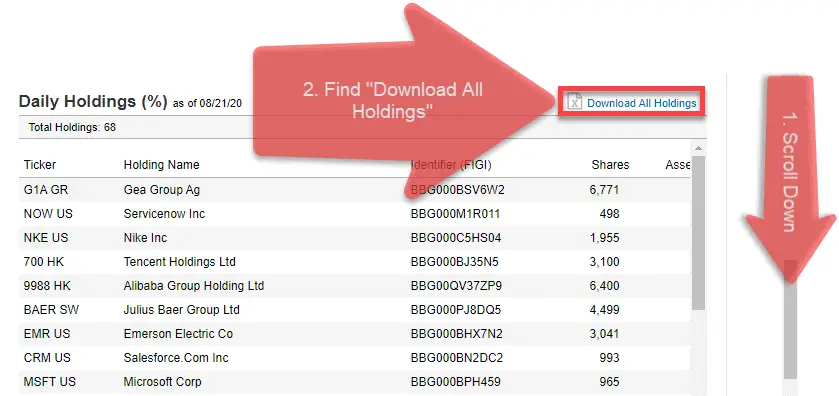

1. Morningstar Wide Moat ETFs

VanEck has ETFs that track two Morningstar indexes that contain undervalued Canadian wide moat stocks.

Check out the holdings of these ETFs to find undervalued wide moat stocks.

- GOAT – Morningstar Global Wide Moat ETF Holdings – Global (including Canada and US) undervalued wide moat stocks

- MOTI – Morningstar International Moat ETF Holdings – Global (excludes US, includes Canada) undervalued wide moat stocks

The links above are geared towards US investors. After you click the link they may ask you which country you are from. If they do, select US. If you don’t select US, the links might not work.

Look for the “Download All Holdings” link to get a spreadsheet of all the current holdings.

2. Canadian Dividend All-Star List (CDASL)

A long dividend streak doesn’t necessarily mean the company has a wide or narrow moat, but it can be an indication of a high-quality company.

The Canadian Dividend All-Star List (CDASL) is a free excel spreadsheet that I email to my subscribers every month. It contains stock information on Canadian companies that have increased their dividend for 5+ years in a row.

Download CDASL

Subscribe to the Dividend Growth Investing & Retirement newsletter and you'll be emailed the download link for the most recent version of the Canadian Dividend All-Star List (CDASL).

3. Morningstar

I used Morningstar’s moat ratings for this article, so check your online broker for Morningstar access. Most Canadian brokers provide it free.

For a list of Canadian brokers that provide Morningstar access as well as some other ways to get Morningstar free, check out the details in my upcoming article: 3 Ways to Find Wide Moat Stocks – Coming December 1, 2020.

Summary

I used Morningstar to find all of Canada’s wide moat stocks.

They provide two types of moat ratings:

- Analyst (real person) ratings, and

- Quantitative ratings (a computer formula figures it out instead of a person).

The quantitative ratings are less reliable than the analyst ratings.

Wide Moat Stocks from Morningstar Analyst Ratings

- Canadian National Railway Co (TSE:CNR; NYSE:CNI)

- Canadian Pacific Railway Ltd (TSE:CP; NYSE:CP)

- Enbridge Inc (TSE:ENB; NYSE:ENB)

- Royal Bank of Canada (TSE:RY; NYSE:RY)

- The Toronto-Dominion Bank (TSE:TD; NYSE:TD)

- Waste Connections Inc (TSE:WCN; NYSE:WCN)

Wide Moat Stocks From Morningstar Quantitative Ratings (These are the less reliable ratings)

- Constellation Software Inc (TSE:CSU)

- Enghouse Systems Ltd (TSE:ENGH)

- Franco-Nevada Corp (TSE:FNV; NYSE:FNV)

Some companies that I thought would be considered wide moat, like the larger Canadian Telecom and Utility stocks, turned out to have narrow moat ratings.

Were you surprised by any companies that didn’t make the wide moat list?

PS. Don’t forget to check out my other wide moat articles:

- What is a Moat? With 5 Canadian Wide Moat Examples

- Why Invest in Wide Moat Stocks?

- 3 Ways to Find Wide Moat Stocks

- Each & Every Wide Moat Stock in Canada (This is the article you just read)

- Every Wide Moat Stock in the USA

- International Wide Moat Stocks – Every Single One Listed

- 8 Canadian Dividend Growth Wide Moat Stocks

- 76 US Wide Moat Dividend Growth Stocks

- 23 International Wide Moat Dividend Growth Stocks

- 100 Canadian Narrow Moat Stocks

- 44 Canadian Wide & Narrow Moat Dividend Growth Stocks

Newsletter Sign-Up & Bonus

Have you enjoyed our content?

Then subscribe to our newsletter and you'll be emailed more great content from Dividend Growth Investing & Retirement (DGI&R).

BONUS: Subscribe today and you'll be emailed the most recent version of the Canadian Dividend All-Star List (CDASL).

The CDASL is an excel spreadsheet with an abundance of useful dividend screening information on Canadian companies that have increased their dividend for five or more years in a row.

The CDASL is one of the most popular resources that DGI&R offers so don't miss out!

Great series

Looking forward to the rest of the series

-Jason Calgary

Thanks Jason!

Excellent resource. Great info, as always!

Thanks Susan!

Fantastic article!! Wide moats make great dividend stocks.

Thanks David!

Thanks for all the information. I assume that Fortis is consider a narrow moat company.

Yeah Fortis has a narrow moat.