Dividend Growth Investing & Retirement is supported by its readers through donations and affiliate links. If you purchase through a link on my site, I may earn a commission. Thanks! Learn more.

One of the reasons I started this blog was to educate others and to improve my own investing. This is why I like to keep my readers up to date on my portfolio changes. I’ve been getting a bit behind with my portfolio updates so this is going to be a catch-up post of four January 2016 transactions that I haven’t discussed yet.

⭐ Find dividend growth stocks that have survived multiple recessions and increased dividends for 5, 10, 25+ years in a row.

By keeping an open book of my portfolio and changes to it, I hope to generate discussion so others can see how I put my investing philosophy into practice. For the most up to date portfolio changes follow my twitter account as I will usually tweet the day I buy or sell stocks and then follow-up with a blog post.

January 20, 2016

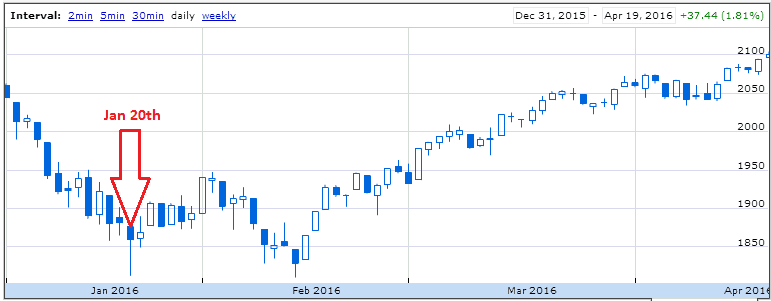

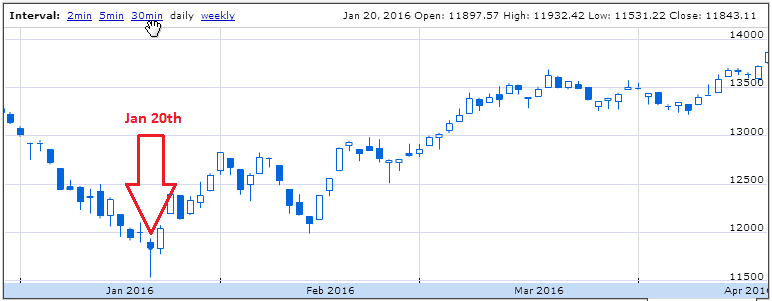

On January 20, 2016 I took advantage of the stock market drop and purchased three companies: IBM [IBM Trend], Enbridge [TSE:ENB Trend], and National Bank [TSE:NA Trend]. I don’t know you if you remember, but January was a pretty ugly month for the stock market. Prices had been dropping for a few weeks, so I placed some orders in hopes that they’d get triggered if the market kept dropping. I got lucky and they were triggered on January 20th. I went back and found a CNN Money news article headline from that day to give you an idea of the sentiment at that time: From horrible to just bad: Dow ends down 249 points. Oh yeah, and oil was $27.

You can see from the following two charts of the S&P 500 index and the S&P/TSX Composite index that January 20th was a low for the month.

Oh what a difference a few months make. Looking back, it just makes me appreciate how important it is to ignore the daily noise and focus instead on long term fundamentals.

Top Ups – IBM & National Bank

International Business Machines and National Bank of Canada were small top up additions to existing positions where I was just hoping to take advantage of low prices and add a few more shares. I purchased IBM at $118.47 plus the commission and National Bank was purchased at $36.00 plus the commission. I’m not going to go into detail about these companies as I’ve already discussed them here:

- Portfolio Update: IBM Purchased

- Portfolio Update – National Bank of Canada & Exxon Mobil Corporation Purchased

New Addition – Enbridge

I purchased a small amount of Enbridge shares at a price of $42.00 + commission. I sold my Kinder Morgan Inc. [KMI Trend] after they cut the dividend so I decided to put some of that money back into another pipeline stock. I don’t plan on adding more to this position as I’m happy with my current energy allocation right now. There are few things I like about this stock and one thing that I don’t.

Things I like:

- Rated a wide moat stock by Morningstar.

- Long history of dividend growth. The company has increased its dividend for 20 years in a row and has 5 and 10 year annual dividend growth rates of 17.0% and 13.6%. The most recent dividend increase was 14% and the company is forecasting dividend growth of “14-15% dividend growth between 2015 and 2019” so it looks like the plan is to maintain this high dividend growth rate. Their payout ratio; which I’ll discuss later, is high so I would temper your expectations as it is hard to maintain high dividend growth rates above 8% for a long time. It’s always good to take forward estimates with a grain of salt.

- High starting forward dividend yield of 5%. In January this was a TTM dividend yield of 4.4% which I compared to the highest dividend yield’s for each year going back to 2003 in the Canadian Dividend All-Star List. In 2015 it got up to 4.65%, in 2009 up to 4.16% and in 2003 up to 4.04%. These were the three highest years. This suggests the stock was cheap from a dividend yield perspective.

- Reasonable financial strength with a stable S&P credit rating of BBB+.

What I don’t like:

- High payout ratio. In 2015 they paid out dividends of $1.86 and had adjusted EPS of $2.20 which is a 2015 payout ratio of 86% – this is high. If you compare dividends to the adjusted cash flow from operations (ACFFO) for 2015 of $3.72 it comes in at a much more reasonable 50%. We’ll talk ACFFO later, but before we do lets look at some 2016 estimates. Analysts are currently estimating 2016 EPS at $2.28. With the increased dividend we can expect 2016 dividends of $2.12 ($0.53 x 4) which works out to an estimated 2016 payout ratio of 93%.

I’ve mentioned ACFFO because Enbridge is using this instead of EPS to determine their target payout ratio. If you look at their website it currently says “Enbridge’s target dividend payout is between 40 to 50 per cent of earnings” which is a little misleading, because they actually mean 40-50% of ACFFO. I found this in the 2015 annual report:

“In conjunction with the execution of the Transaction, Enbridge adopted a supplemental cash flow metric, available cash flow from operations (ACFFO), which was introduced in the second quarter of 2015 and is now a part of the Company’s normal course annual and quarterly reporting of financial performance and in the provision of guidance. ACFFO is used to assess the performance of the Company’s base business and the impact of its growth program. The Company also started expressing its dividend payout range as a percentage of ACFFO rather than adjusted earnings and has established a long-term target payout of 40% to 50% of ACFFO.“

As this is a pipeline company I can’t help but remember the not too distant past when I got burned by a Kinder Morgan Inc. dividend cut. Rather than ACFFO Kinder Morgan used distributable cash flow (DCF) instead of earnings to determine dividend payout ratios. A payout ratio based on earnings is more conservative as it takes into account depreciation and a few other things that in the long term you will eventually have to deal with. When Kinder Morgan Inc. cut its dividend its payout ratio based on earnings was sky high and its payout ratio based on DCF was basically at 100%. Now I’m not expecting Enbridge to cut its dividend, as we are not at those same levels, but it I’d be lying if I wasn’t a bit nervous that they use ACFFO instead of EPS. If you think I’m out to lunch, please comment as I’m curious if others think the payout ratio with Enbridge is currently high.

Overall I’m happy with the Enbridge purchase, but I’ve lowered my dividend growth expectations from management’s 14-15% per year because of the high payout ratio.

That wraps up a busy day of buying shares for me. The next transaction was a the sale of a stock on the 28th.

January 28, 2016

On January 28, 2016 I sold Potash Corporation of Saskatchewan [TSE:POT Trend] after they announced their first dividend cut since their 1989 IPO. The dividend was cut approximately 35% to $0.25 per quarter. I originally bought shares of Potash twice in September 2015 for an average price of $27.75. I sold these shares for $20.71 less the commission. This was a loss of about 25.4% less the dividends I received.

Related article: Portfolio Update – Potash Corporation of Saskatchewan Purchased

It always stings loosing money, but as a dividend growth investor I chose to bite the bullet and sell Potash when they announced their dividend cut. My investment plan relies on growing dividends over time. It doesn’t make sense for me to hold on to companies that cut their dividend so Potash was sold.

Related article: In What Conditions Would I Consider Selling A Stock?

I went wrong with my initial purchases of Potash by chasing a high yield with a high payout ratio for a basic materials company. Typically basic materials need a low payout ratio to operate efficiently. At the time I was happy to be able to add a basic materials company as it diversified my portfolio into a new sector and I thought they wouldn’t cut the dividend because they never had before in the company’s history. I was wrong and had to sell.

That wraps up my investing activity for January. What do you think of my purchases? Would you have sold Potash after the dividend cut, or held on?

Disclosure: I own shares of IBM, Enbridge, and National Bank of Canada. See my portfolio here.

Photo credit: Gruenewiese86 via Foter.com / CC BY-ND

Newsletter Sign-Up & Bonus

Have you enjoyed our content?

Then subscribe to our newsletter and you'll be emailed more great content from Dividend Growth Investing & Retirement (DGI&R).

BONUS: Subscribe today and you'll be emailed the most recent version of the Canadian Dividend All-Star List (CDASL).

The CDASL is an excel spreadsheet with an abundance of useful dividend screening information on Canadian companies that have increased their dividend for five or more years in a row.

The CDASL is one of the most popular resources that DGI&R offers so don't miss out!

I enjoy visiting your site and observing your stock watch list. One area that I am interested in is the selling point of a stock. I notice that your watch list displays realistic buy price targets. Do you also calculate selling price targets?

Sorry if I missed this information or link on your site. If you have selling targets on your site could you please provide a link so I can observe this information. Thanks.

Hi Joe,

I don’t typically calculate a selling price target. You can read about the conditions I typically sell a stock here.

My purchase on POT was around $27 as well but still holding it. It is around $20-21. I will wait it out and probably average down a bit going forward. Congrats on IBM and National banks!

Wouldn’t you consider averaging down as the business is cyclical it will kick back up further done the road especially with the fundamentals in place (growing population and less growing spaces). I don’t expect the conditions in the short term to get any better for the company as supply exceeds demand at this time but down the road if your entry point or average cost is low that would mean a higher yield once the cash flow kicks back up? I know this is highly speculative but since the company has a history or returning a majority of its profit to shareholders there is more chances they hike then cut the dividend in the long term. I foresee and entry point if they cut the dividend once more after a few more bad quarters.

Your thoughts?