Dividend Growth Investing & Retirement is supported by its readers through donations and affiliate links. If you purchase through a link on my site, I may earn a commission. Thanks! Learn more.

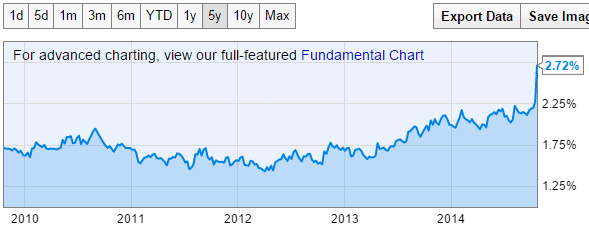

IBM [IBM Trend] is one of those stocks that I didn’t think I’d get to own because of its low yield, but in the past 5 days the stock price has dropped 11%, so I was able to initiate a position with a dividend yield of 2.7%. I typically like to invest in companies with a dividend yield of at least 2.5%. Going back to 1999 there have only been two years where the highest dividend yield was above 2.5%. In 2008 the highest dividend yield was 2.7% and in 2009 it was 2.6%. To be able to buy in at a yield level similar to when the financial crisis was going on, is enticing. While 2.7% isn’t the highest dividend yield, it is high for IBM. Take a look at chart below and you can see that historically this is a high dividend yield.

⭐ Find dividend growth stocks that have survived multiple recessions and increased dividends for 5, 10, 25+ years in a row.

Yield isn’t the only value metric that looks enticing for IBM, its P/E is currently 10.2 according to MorningStar. Not to mention Warren Buffet is an investor having purchased shares a few years ago around $170. It feels good to buy in at prices below one of the all-time great investors.

I’ve talked a bit about why IBM appears value priced, but I should also probably talk about what is causing these deflated prices. The price dropped because IBM lowered their guidance and came out with lower than expected earnings. In the past management was targeting $20 of EPS in 2015, but they no longer think this is possible. While the latest quarter was disappointing I took this disappointment as an opportunity to buy IBM at deflated prices. I purchased shares on October 22, 2014 for $162.54 + commission.

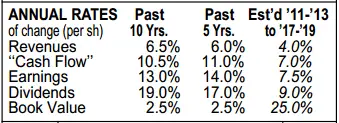

I think there are some valid worries about revenue growth, but I think the good outweigh the bad in this case. For instance Valueline is estimating annual dividend growth of 9% for the next 3 to 5 years.

Here are the bullets of why I purchased IBM:

- 5 and 10 year dividend growth rates of 14.3% and 19.4% according to David Fish’s September 30, 2014 US Dividend Champions list.

- Sustainable growing dividend with a payout ratio around 30% and a dividend streak of 19 years.

- Strong financial strength. Valueline has an A++ financial strength for IBM.

- History of increasing earnings and dividends at double digit rates.

- The stock appears value priced.

- Wide economic moat according to MorningStar.

Conclusion:

I struggled a bit with this purchase because I’m using the Smith Manuever which means I’m borrowing to invest. My interest rate is 3.25% so the starting dividend yield is below this. Long term I expect the dividend to grow and my yield on cost will grow above the interest rate. My portfolio as a whole will include a mix of lower and higher yield stocks that will likely end up with a portfolio yield of around 3-4% based on the type of stocks I invest in. Investing in technology stocks when you plan to hold onto the stock for forever can be risky because technology changes at a rapid pace, but IBM has shown it has the ability to pivot well in a changing landscape. At the end of the day while certain things about IBM make me nervous, I’m content with my investment. IBM has a strong dividend growth history that I expect to continue sustainably, a wide moat, strong financial strength, and the stock appears to be on sale. These are the markings of a good dividend growth investment, which is why I bought shares.

Photo credit: Looking Glass / Foter / CC BY-SA

Newsletter Sign-Up & Bonus

Have you enjoyed our content?

Then subscribe to our newsletter and you'll be emailed more great content from Dividend Growth Investing & Retirement (DGI&R).

BONUS: Subscribe today and you'll be emailed the most recent version of the Canadian Dividend All-Star List (CDASL).

The CDASL is an excel spreadsheet with an abundance of useful dividend screening information on Canadian companies that have increased their dividend for five or more years in a row.

The CDASL is one of the most popular resources that DGI&R offers so don't miss out!

Im surprised you are buying American companies for the Smith Manoeuvre. I don’t disagree about anything you said in your decision to buy, but in addition to the yield being lower than your HELOC interest rates, you will also be dinged withholding taxes of 15% of the dividend. Smith Manoeuvre investments can’t be held in registered accounts so there is no way to shelter from this loss. I know there are good odds ibms divvy growth will catch up but are you buying American companies for their solid div growth despite the 15% loss of dividend forever?

@Erich

I also do not hold any US stocks outside of my RRSP’s. Even in a “registered” TFSA you would get dinged with witholding taxes. Heck I even got dinged with taxes in my RRSP because although i bought on a US exchange they were a foreign company Royal Dutch Shell (I’ll let you guess which country). Also MLP’s (KMP) get dinged within RRSP’s as well – over 35% tax. It happened to me and that is why I sold out of KMP. I now own KMI

As to running a HELOC to perform the Smith manuever it is a good use of the HELOC as all interest charges will now be tax deductible. I do question your 3.25% charge though. You should be able to get 3%. Just go and tell them other banks offer it. That is what I did and went from 4.25% to 3.5% to 3% – all because I heard of it on the radio and went in and asked my bank why they were not offering the same rate to me. Did it twice and each time they had it all done by the next week.

As to buying IBM??? My personal opinion is 1) it is really expensive monetary wise. By that I mean you could have bought ten different stocks @ $16 and you would have been much more diversified. Or a JNJ and KO as similar or better divs. 2) Buying US stocks brings in to play curreny exchange rates. Nice when our $Cdn is going down but not so nice if it appreciates from your COP. I doubt if we will see much apprecaiation above $0.90 and probably more likely to head a bit lower. 3) my personnal feeling about IBM is that it was a great company but they are under going a long term restructuring from a manufacturer to a software implimentation company. My personal crystal ball has told me (LOL) that there is more long term downside to IBM than upside. But my crystal ball has been wrong before telling me Nortel was a good solid company. Lost a few dianro there. But that is just personal opinion and yours is just as valid as mine and really more valis as it is your opinion and your money.

Take care. Good investing

RIchard

I had a really hard time finding anyone that would offer less than 3.5% when I was looking. I know CIBC right now is offering 3.0% as an introductory rate, but then they increase it back to 3.5%. I spoke with a few mortgage brokers and various financial institutions and the feeling that I got was that it is harder to get 3.0% right now, whereas in the past it was more common place. It’s not like I don’t have good credit, I just think the banks have tightened up a bit. When did you get yours lowered to 3.0% from 3.5%?

Interesting that you bought the IBM shares with Smith Manuever but I can understand your reasons behind the purchase. Nice buy!

(I sent this by reply email; should have posted it here instead. So here goes.)

If IBM’s current dividend yield grows at the estimated forward rate of 9% per year, in ten years you’ll have a yield on cost (YOC) of under 4%. Is this your (author’s) goal?

By the way, if I buy a bunch of stocks, keep them forever, and their dividends grow enough to provide a portfolio YOC of 10% within ten years, that’s great. That’s my goal. But that’s not reality, for two main reasons.

First, I will have to sell some stocks and start over at a dividend yield of about 2.5% – 4%. I suppose I can keep the portfolio YOC at (e.g.) 10% by using the capital gains from sale of stocks to buy additional shares in the new stocks. The initial YOC will be lower for the new stocks, but the income from additional shares will the overall portfolio (dividend income divided by total capital invested) will remain the same 10% or better. So, no problem here after all.

But reason (2) seems to present a problem. I will presumably invest more capital into the portfolio over time, which increases the denominator in the calculation of portfolio YOC. The new money will have to go into new stocks at initially lower dividend yields, and this will lower the portfolio YOC.

So, is my goal of a portfolio YOC of 10% after ten years unattainable unless I stop adding more capital?

A yoc goal of 10% is generally based on 2 factors:

1. Growth of the dividend on top of initial purchased yield compared to initial cost

2. Reinvestment of the dividends received which are not calculated as your contribution so do not increase your cost basis.

Some people reinvest all dividends back into the original company, but many will instead gather all received dividends and purchase either a new position or add to whichever existing one has the best valuation.

Therefore yoc goals are generally applied to a whole portfolio. Obviously the calculation of this goal is not straightforward with ongoing contributions but that does not mean the same stock selection process cannot be applied to dividends and new contributions.

You could take a snapshot of portfolio on a given day and calculate with reinvested dividends of the portfolio 10 years later to get a reasonable estimate of your results, or even open a new account if you want to be that picky about accurate results. There are people on seeking alpha with real demo portfolios with no new added money proving the concept now.

I don’t have a set yield on cost goal for myself. For IBM after 10 years I get a yield on cost of 6.4% [2.7% x 1.09^10].

Yes, my Sharp business calculator agrees IF you set the calculation to “Begin”, which means the entire dividend is received at the beginning of the year. If you’re spending the dividends, it makes little difference when you receive the divs — at the beginning or the end of the period N. But if you’re re-investing the dividends to increase the portfolio, then when you receive the dividends (beginning or en of the period) makes a large difference when compounded over ten years. I’m sure you know this better than I.

A more precise calculation would be to receive the dividends in 4 tranches during the year, and assume that each tranche is received at the beginning or at the end of that period. The YOC in ten years would be lower. But no matter if you don’t have a particular YOC goal.

I am curious, though. If the overriding purpose of a dividend-growth portfolio is to produce income above a given threshold, and if thee are other stocks just as solid as IBM and likely to produce higher YOCs, why not choose them?

While the purpose of my dividend growth portfolio is to produce income, it is not the only consideration I take. In order to better protect my investment I like to buy stocks when they go on sale or below a price that fits my risk-reward appetite. It is not my intention to sell these investments, ideally I will hold them forever and collect a growing stream of dividends. In reality things come up that you can’t plan for and I may need the money. For instance we recently bought a place. To come up with the down payment I sold my stocks. While I’m not expecting to have to sell in the future there might arise a situation where I need to access the money. I have an emergency fund, but you can only plan so much. My strategy is focused on dividend growth with elements of value investing you could say. The elements of value investing are to protect myself better from significant drops in price.

So if other stocks are just as solid as IBM and likely to produce higher YOCs, why haven’t I chosen them? The short answer is they haven’t dropped enough in price. I have target buy prices and once a stock goes below it, I will consider investing in it. I set these target buy prices fairly conservatively, which limits my investing options, hence why I haven’t bought other higher yielding stocks instead of IBM.

Good answer. Thank for the perspective.

Hi DGI&R;

Approx two years ago for the 3% Heloc.

One thing to keep in mind is that they want to keep your business, especially it they are making money from it. If you mention that you can get 3% at another financial institution they will jump on it. A lot may depend on your financial position. I had a mortgage free house to put up a collateral (where is their risk?) so getting 3% was, so to say, better than nothing or worst losing me to another bank.

Again, my daughter was able to get a better deal than me with absolutley no collateral and student debts. So push them to the wall. They are there to make money and they do not want to lose you. Even better if you own some of their stock so therorectically you are paying yourself.

The bank ended up lowering my rate from 3.5% to 3.0% after all and I didn’t even have to bug them, which was nice. Since then prime has dropped, and I’m now getting 2.85% which seems to be in-line with other banks.

I just picked up some shares of IBM this am in fact. I think the selloff was overblown but I know that IBM is still facing some issues. They need to get back to growing but the good thing is that they’ve kep their balance sheet clean so they can afford to try new things for the business and still stay in great financial shape.