Dividend Growth Investing & Retirement is supported by its readers through donations and affiliate links. If you purchase through a link on my site, I may earn a commission. Thanks! Learn more.

One of the reasons I started this blog was to educate others and to improve my own investing. This is why I like to keep my readers up to date on my portfolio changes. For the most up to date portfolio changes follow my twitter account as I will usually tweet first and then follow-up with a blog post. By keeping an open book of my portfolio and changes to it, I hope to generate discussion so others can see how I put my investing philosophy into practice.

⭐ Find dividend growth stocks that have survived multiple recessions and increased dividends for 5, 10, 25+ years in a row.

Canadian Utilities Limited Purchase

On December 8, 2015, I purchased shares of Canadian Utilities Limited [TSE:CU Trend Analysis] for $30.00 per share plus the commission. The company is a utility company engaged in the transmission and distribution of electricity and natural gas. They are also engaged in power generation and sales, natural gas gathering, processing, storage and liquids extraction. I purchased shares in this utility company for a number of reasons:

- According to the Canadian Dividend All-Star List, it has the longest dividend streak of any Canadian company at 44 years of consecutive dividend increases. Not too shaby!

- It has a history of high dividend growth that I expect to continue. Canadian Utilities has 5 and 10 year average annual dividend growth rates of 9.3% and 7.9% respectively and in January 2016 they announced a 10% dividend increase. Analysts are estimating that they’ll earn $2.16 in 2016. With the current annual dividend for 2016 at $1.30 this puts the payout ratio around 60%, which is reasonable for a utility company.

- It has a high dividend yield. When I bought shares it was yielding 3.9%, but they announced a dividend increase shortly after that I was expecting so my yield on cost is currently 4.3%.

- Shares appeared reasonably cheap at $30. The dividend yield and price/cash flow were at levels similar to the third cheapest year in the past decade. In 2009 the dividend yield reached 4.13%, which was the highest in the past decade. In 2003 the dividend yield reached 4.52%. At $30 the dividend yield was 3.93% (December 2015) which is not far off.

- It has strong financial strength. Both DBRS and S&P give them a credit rating of “A”.

- My portfolio didn’t have any exposure to the utilities sector. Most of my recent purchases have been in the energy and financial sector, so it was nice to diversify beyond these sectors.

Atco vs Canadian Utilities

Atco Ltd [TSE:ACO.X Trend Analysis] owns 53% of Canadian Utilities so naturally before I made my Canadian Utilities purchase I considered buying Atco. Both companies were trading at what I considered to be historically cheap, but ultimately I picked Canadian Utilities because it was more of a pure utility company and had a higher dividend yield. Atco has utility exposure through its ownership in Canadian Utilities, but it also operates a Structures & Logistics (manufacturing, logistics and noise abatement) business line. Utility companies typically have regulated, but long contracts which results in a fairly reliable stream of income. As this reliable stream of income grows the company is able to increase the dividend. This is why I was more interested in the utility side of the business versus the structure & logistics side.

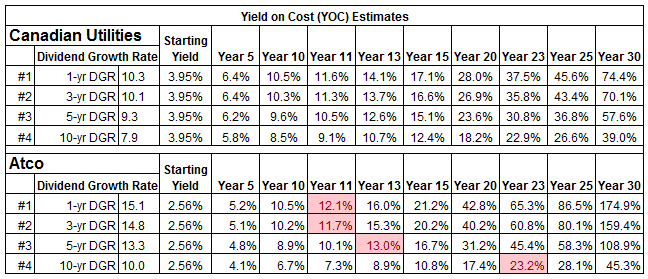

Canadian Utilities has a longer dividend streak and typically has a higher dividend yield. While Atco has a shorter dividend streak of 22 years, this is still a long dividend streak, so this didn’t factor too much into my decision. The higher dividend yield did though. You can see from above that on December 8th Canadian Utilities had a yield of 3.95% versus Atco’s 2.56%. There is an argument to make that while Atco’s dividend yield is lower its dividend growth is higher. I ran a few yield on cost tests based on this argument.

I estimated the future yield on cost using the 1, 3, 5, and 10 year dividend growth rates of each company. You can see from the above chart that it is not until year 11, 13, or 23 that Atco would have a higher yield on cost. Historically it is difficult to maintain high dividend growth rates for these periods of time, so rather than hope that such a high dividend growth is maintained, I opted for the higher current yield of Canadian Utilities. In my opinion Canadian Utilities offered a good mix of high current yield and good dividend growth potential as evidenced by their recent 10% dividend increase announcement in January 2016.

Related article: Can Past Dividend Growth Rates Be Relied Upon To Predict Future Rates?

Final Thoughts

Because Canadian Utilities is based in Alberta I thought the turmoil there might cause the stock to continue to drop. I originally bought a 50% position in Canadian Utilities with the idea that if it dropped further I could pick up some more shares, but it has since increased by ~20%, so it doesn’t look like I’ll be buying more shares for the time being. If Canadian Utilities drops to $27 then I’ll consider buying more shares to bring this up to a 75% position. Alternatively if Atco dropped to $29 before Canadian Utilities dropped to $27, then I’d consider buying a 25% position in Atco instead. I’d be fine owning both companies, but because Atco owns a lot of Canadian Utilities I’d want to keep the allocation of both stocks combined to a full position for one stock.

What do you think of my recent purchase of Canadian Utilities? Would you have bought Atco instead?

Newsletter Sign-Up & Bonus

Have you enjoyed our content?

Then subscribe to our newsletter and you'll be emailed more great content from Dividend Growth Investing & Retirement (DGI&R).

BONUS: Subscribe today and you'll be emailed the most recent version of the Canadian Dividend All-Star List (CDASL).

The CDASL is an excel spreadsheet with an abundance of useful dividend screening information on Canadian companies that have increased their dividend for five or more years in a row.

The CDASL is one of the most popular resources that DGI&R offers so don't miss out!

What do you think about Fortis? As I understand it it is cheaper than CU, bit with thé same profile.

I like Fortis, but I don’t start to get interested until around $33. This will likely keep me on the side lines for now. When you say cheaper, by what metric?

Looks good.

How did you get the dividend history? Yahoo Finance doesn’t list CU. CU’s website gives the dividend history only in the form of a bar chart, without specific dividend prices.

In calculating the future YOC, why do you use the 5-year dividend growth rate (instead of, say, the 3-year growth rate, or the 10-year rate)? Just curious. I use the lowest of the rates for my calculations, but perhaps that is being too conservative.

TSX listed stocks have the .TO suffix on Yahoo Finance. The dividend history is available in many places, for example, on CU’s website, Yahoo, Google Finance, Dividendinvestors.ca, dividendhistory.org and on this site on the Canadian Dividend All Star list.

Hi Len,

For the YOC estimates I used the 1, 3, 5 and 10 year dividend growth rates and ran four different scenarios (listed as #1, #2, #3, and #4 in the table in the article). These tests weren’t about deciding which was the most accurate or most conservative, it was about comparing each of these 4 tests to the same Atco test to see when Atco might have a higher yield on cost. In the end based on the 4 scenarios it meant that Atco wouldn’t have a higher yield on cost until 11 to 23 years later.

I think taking the lowest of rates is a good conservative approach for estimating future yield on cost. If the lowest rate is high say 20% do you still use this in your future yield of cost estimates or do you pick a smaller number as these really high rates are very difficult to sustain for the long term?

Cheers,

DGI&R

Len, here’s another potentially useful site re: dividend sleuthing.

http://www.longrundata.com/index.php

For Cdn. symbols the .tsx is used — ie. Cdn Utilities is CU.tsx

You can change the start & end dates being considered to calculate dividend growth rates. The longrundata site also details the previous 8 dividend payments and dates.

Hope it helps. Dividend growth takes time but it does work, especially if buying happens at/below long-term “normal” pricing levels. For many situations we seem to be on that part of the pendulum now and probably for a while longer too.

Further thoughts on CU.

It is on a downtrend, trading below its 200 day EMA (usually not a good sign). So, even at $30 per share, it would be risky to buy, until it seems again on an uptrend. Why not wait until it bottoms out and is again on a convincing uptrend (i.e. the 100 EMA is above the 200 EA)?

Credit Suisse has downgraded CU from outperform to neutral — despite the (to me at any rate) solid fundamentals reported in TD’s Web-broker. I’d want to know why before buying.

The dividends seem inconsistent. I asked before where you got the dividend information from. This question is even more important now that I see Web-Broker showing a dividend of .4025 per share in April 2011, rising to .4850 in April 2013, but the declining to .2425 in July 2011.

Inconsistent dividends make it doubly difficult to project future YOCs. .

Canadian Utilities has a pretty consistent dividend streak. It looks like Web-Broker didn’t take into account the 2 for 1 split. You have to watch out for this as I’ve seen this happen with a few different sources quite a bit and it can be misleading. From Canadian Utilities website: “On June 14, 2013, Canadian Utilities effected a two-for-one share split.”. The April 2013 dividend of .4850 after the split would be equivalent to .2425 and then the July 2013 (I’m assuming you meant 2013 and not 2011) dividend of .2425 would be the same level of dividend which makes sense because they usually increase with the 1st dividend of the year and keep the other dividends at the same level.

When I calculate the dividend streaks and look at prior dividend history I look at a variety of sources to get the information, but if it is not easily available on the company’s website then this usually means combing through the annual reports or annual information forms on http://www.sedar.com.

When it comes to momentum investing, I don’t know very much on the topic. At this point I haven’t looked into it enough to know if it will help me time the market. I bought Canadian Utilities because I’m a long term investor and I think at $30 it offers me good value. It could drop further below that, but I’m of the opinion that I can’t predict the future. If I see what I think is a strong dividend growth stock trading at a reasonably cheap price I will typically buy it and hold it long term. This might mean my portfolio is more volatile that yours, but I’m OK with that as I’ll get more opportunities to buy great companies than you, if you have to wait for the trend to be up.

The other thing that I wanted to point out is that by waiting for the stock to rebound and only buy as it goes up you may be missing out on a good portion of the returns. I’d be curious to know what the effects of the lost opportunity costs of this strategy are on long term returns? I got this from Investopedia:

Timing

When it comes to market timing, there are many people for it and many people against it. The biggest proponents of market timing are the companies that claim to be able to successfully time the market. However, while there are firms that have proved to be successful at timing the market, they tend to move in and out of the spotlight, while long-term investors like Peter Lynch and Warren Buffett tend to be remembered for their styles. Figure 2 below shows returns from 1996 to 2011.

Source: SchwabCenter for Financial Research

Figure 2: S&P 500, 1996-2011

This is probably one of the most commonly presented charts by proponents of passive investing and even asset managers (equity mutual funds) who use static allocation, but manage actively inside that range. What this data suggests is that timing the market successfully is very difficult because returns are often concentrated in very short time frames. Also, if you aren’t invested in the market on its top days, it can ruin your returns because a large portion of gains for the entire year might occur in one day.

If you missed the top 10 days in the market for the year your returns would be significantly smaller. I’m not saying your strategy misses these days, by waiting for the uptrend, but you do miss out on some opportunities to invest. Over the long term, by not investing in these companies that you missed because of a lack of uptrend would you have been better off investing in them vs not? Food for thought.

It sounds like we have different entry criteria which is fine. I hope I didn’t come of as too preachy in this comment I genuinely like it when people ask me difficult questions and I have to answer them. It makes me a better investor.

Cheers,

DGI&R

I couldn’t get the picture of the table to show properly in the comment, so you’ll have check out the link to investopedia: http://www.investopedia.com/articles/stocks/08/passive-active-investing.asp.

The table is from a study of the S&P 500 from 1996 to 2011. The S&P 500 index returned 7.8% per year on average during this time. If you exclude the top 10 days the returns are 4.1% per year. Exclude the top 20 days and it is 1.7%, exclude the top 30 days and it is -0.4% and exclude the top 40 days it is -2.3%.

Me too; I like an intelligent exchange of viewpoints; this make me a better investor too.

I normally look askance at conspiracy theories, but if there is one I give more credence to, it’s the one that holds that Wall Street and mutual fund companies want investors to invest their money and go away, not create waves by buying and selling consistently. And brokers want the money invested, not sitting I cash, because they are paid on assets under management, and cash is not managed.

But set this aside.

The point that gains are concentrated in a few days is sort of true, despite the saying that the market goes up by the stairs and down in the elevator – i.e. gains are gradual, while losses are sudden and dramatic.

I once put this theory to the test, and found that yes, missing the top ten gains really depressed CAGR. But I also found that missing the ten worst days improved CAGR more than missing the top ten depressed CAGR. Clear as mud? It means that being in cash, missing the worst ten market days is good for CAGR, even if it means missing the best ten days as well.

In other words, there is plenty of profit to be made in the middle ranges, between top and bottom – AS LONG AS there is a large difference between top and bottom. Furthermore, I used my technical indicators to compare my timing system with buying and holding SPY, from 2000-2016. The timing system had a modest 7 transactions during this 16-year period, and handily outperformed Buy&Hold. I will explain this system – a very simple one – to those interested enough to request it. I won’t gum up this site with an explanation; I will send to individual email addresses.

Thanks for sharing Len. Do you use your momentum strategy to help determine when to enter a position and then hold on to it, or do you sell based on momentum to?

Len Petry, I would be interested to read about your Timing System, trying to make significant gains, Buy and Hold doesn’t cut it for me.

Invest if the MACD (100/200 20 day smoothing) is positive, and the 100 day EMA is above the 200 day EMA, invest.

Go to cash if the 100 day EMA crosses down below the 200 day EMA. Ignore the MACD for selling signals (it gives too many sells/buys, hence you get whipsawed).

Results for the testing period of 1 Jan 1996 to 9 February 2016, a period of 20.12 years.

I chose 1 January as the starting date arbitrarily, to avoid any controversy about cherry picking dates. Then I “cashed out” on the day of analysis, 9 February 2016.

Buy&Hold (B&H) had only one transaction, of course, because with B&H you are never supposed to sell. (Of course, the B&H investor must eventually sell something in order to live on his portfolio during retirement, but let’s not get bogged down in nitpicking.) In contrast, Timing had 10 transactions – an average of 1 every two years – for a total commission cost of $49.50.

Once set up, a matter of a few minutes, looking at the charts is a matter of a few minutes per day, or per week if you prefer.

The results (the envelope, please). B&H (of SPY) had an annualized return of 9.89%. In contrast, Timing had an annualized return of 12.84%. I didn’t measure volatility, but just looking at a price chart you can see that the Timing system avoids a large part of severe bear markets.

As of 9 Feb 2016, the Timing strategy is in cash, waiting for the market to declare whether we’ve reached a bottom or there is further misery to come.

I use this strategy in a foreign brokerage account, focusing on international ETFs. I use this system with index ETFs, but also other broad specialty ETFs like XLU, and FXY . And I use this system as a guide to when to buy dividend-growth stocks in my Canada account. But in the Canada account I don’t then sell these dividend stocks if the indicators turn south, because my dividend stocks are mainly Canadian stocks (to get the benefit of preferred tax rates on Canadian dividends), and there are not very many quality Canadian dividend growth stocks available. So I hang onto my Royal Bank stocks and my Suncor stocks (yes, I know, I know!) waiting for them to recover. Only if they fool with the dividends, or their financials deteriorate do I consider jettisoning them.

If Canadian dividend stocks I like decline enough to give me a 10% YOC in ten years (I calculate the amount and set an alert for when each stock reaches the right price) , I put them on a watch list and wait for the indicators to go north again, then I buy. For this purpose, the analyses in this site are very useful.

Hope this helps.

@Grrumpy Mac I’d highly suggest you check Fastgraphs, it’s one of the most visual methods of determining a stocks value. Like with any system it has it’s limiations but it’s well worth the 10 bucks a month they charge for it/

I also purchased in the past month and plan to layer in more later. This is an excellent time to purchase a wonderful dividend growth stock which is seldom value priced!

When I compared CU and Fortis in december if I recall correctly CU hade a p/e of over 20 while fortis had 15.

DGI&R said:

“I think taking the lowest of rates is a good conservative approach for estimating future yield on cost. If the lowest rate is high say 20% do you still use this in your future yield of cost estimates or do you pick a smaller number as these really high rates are very difficult to sustain for the long term?”

I HAVE actually been using a high growth rate to calculate YOC, where it was the lowest of the 1,3,5 and 10 year rates. But now that you ask, I am not sure that is always a good idea.

As you mention, high growth rates are hard to sustain. If the dividend growth rate was 35% over ten years, only 20% over three years, and back up to 25% in the latest year, I WOULD comfortably use 20% to calculate YOC. But if the lowest rate (20%) was for the latest year, I might worry that the trend was going to continue downward, and use a lower growth rate for YOC. What this invented growth rate should be I don’t know.

Bernie: Thanks for the sources.

DGI&R, I really appreciate the work that you do and making it available to us. You didn’t mention payout ratios in your piece. Is it something your considered? Thanks Alan

I consider the payout ratio. I mentioned it in the article. Based on 2016 earnings estimates and the 2016 dividend payout ratio is about 60%. Or did you mean I didn’t compare CU’s payout ratio to ACO.X?

yes the differences between the two. No biggie

Well written article!

Both Canadian Utilities and Atco are a part of my portfolio.

As you mentioned in the later part of your post for CU, many Canadian stocks have been affected by Alberta’s economic downturn. At the moment, I really think some of them represent great buying opportunities especially solid long-term contenders like CU.

Yeah I was pretty pleased to be able to buy Canadian Utilities.

What other conpanies are you looking at in Alberta?

Even thought their activities in not concentrated in Alberta, Enbridge (ENB) and Trans-Canada (TRP) are two good examples. Falling oil prices and Alberta’s overall economic turmoil have affected these Alberta based stocks but in the long run, their rock solid structure and diversification both geographically and product-wise should assure us of good long-term returns.

Other “bad news” also affected these two like Keystone and Energy East projects difficulties. I think these news only make them even cheaper and they should still prevail long-term.

If the financial sector, I’m starting to look at Canadian Western Bank (CWB). CWB is a bit more concentrated in Alberta so its price has declined even more. Again, the company looks solid and should be back on its feet after the dust settles. So far, I liked the big banks better but CWB sure is interesting at this point. My portfolio is pretty diversified and mature so I could afford I riskier play like CWB,

Speaking of risky play, I bought Home Capital Group (HCG) in 2015. I think my move was a bit premature as HCG has continued to fall (a lot) since. Maybe buying HCG was a bit too risky for my taste. I’ll still remain patient for a little while but my patience is running out which is pretty rare in my case.

How did you purchase it at $30? I can see the price on Feb 8 didn’t go below $35: http://www.theglobeandmail.com/globe-investor/markets/stocks/summary/?q=CU-T

I’m just starting to invest and am wondering if I’m looking in the wrong places to buy stocks…

I purchased it on December 8th.

Morning,

Missed December (good timing!) bottom, considering both, leaning to CU. Question buy now or wait to Feb. 25 for earnings report?

Waiting for an earnings report may be prudent for trading but I buy stocks for the very long term. IMO the best time to buy a stellar dividend growth stock like CU is on the announcement of their latest dividend increase. CU announced their 10% increase on Jan 7th.

thanks, for direction.

Payout ratio is 75% right now on finance.yahoo.com It seems a bit high…

good discussion & quality writeup. As always, thanks for sharing.

Noticed TRP increased qtrly dividend today from .54 to .565 Home Capital also upp’d their qtrly from .22 to .24 Dividend growth in action…

Not sure if this link below will work, it’s an 83 pager adobe from just over a week ago re: beemo initiation of coverage of 5 midstream situations. Reason for link is that there is some mention of metrics for energy infrastructure situations including some of the power & utilities where Canadian Utilities plays.

fwiw & thanks again for sharing the dividend growth ideas and rationale. Useful information.

http://research-ca.bmocapitalmarkets.com/documents/AC25455D-E48C-4602-9FBF-EC98CBFE2B10.PDF

DGI&R asked:

“Thanks for sharing Len. Do you use your momentum strategy to help determine when to enter a position and then hold on to it, or do you sell based on momentum to?”

No, once bought, I hold onto the stock unless something really negative happens. I am essentially a dividend-growth investor; I just use momentum principles for the entry point.

Actually, I am a true momentum investor with a different part of my portfolio, which comprises International ETFs. With them I do buy AND sell according to my momentum indicators. In that portfolio I am currently in cash mainly, with about 30% in TLT [bonds] and XLU [utilities].)

Back to the dividend-growth stocks. Even where stocks decline seriously, as with some of the bank and oil stocks, I remind myself that I bought them principally because they were able to maintain their dividends through the 2007-1009 period, and so should be able to maintain them this time as well. In fact, I consider this period a good opportunity to buy more shares at good prices. In this I am willing to deviate from my goal of diversification and overweight the beaten-down sectors.

I like the purchase. Just recommended it to a friend I am helping out with her investing, and she bought it a few weeks ago. It is on my watchlist, but right now there are a few others ahead of it. Very likley it will take a bit of a hit when/if rates rise, but long term I think it is a good addition.

I used to own both of Atco and CU but sold off CU when it gained 15-20%. Just holding Atco now. Both are amazing dividend grower but I realized that I was overextended on Utilities a bit. Reduced it to more comfortable level. Your analysis is as always, well thought out. Thanks for sharing!

Cheers!

BeSmartRich

I think now is the time to buy as stocks globally have seen a bit of a dip lately. I agree with John above – a payout ratio of 75% is unreasonably high for the long term…

Can anyone explain how REITs manage to sustain payout ratios of over 100% for years?

With a REIT rather than looking at earnings and payout ratios you look at FFO and AFFO, and those generally tend to be in the 85-95% range. Secondly they are required to pay out the bulk of their earnings each year.

Hi, thanks for the interesting article and comments. As for the dividend growth rate to use for YOC calculations, one can use the estimated dividend growth rates given by ValueLine in their PDF company reports (usually they give a 4-6 year estimate). Access to ValueLine may be offered by your municipal library. In Qc, we have access to it through the BAnQ (national library of Quebec).

Hi Marc:

Has anyone ever checked Valueline estimates of dividend growth rates against reality?

I am open to using them if they have been reasonably accurate in the past.

I currently use past div growth rates (the lowest growth rate to be conservative), to calculate YOC in , 10 years. My goal is 10% YOC in ten years.

The only problem with this calculation is that where the company has not raised its dividend much in the past year (e.g. oil stocks like CNQ and SU), the growth rate is low or flat, and so stock price has to fall to drastically low prices before I can get a YOC of 10% in 10 years. That means I miss good buying opportunities.

So, again,, are the Valueline estimates accurate?

I’m not aware of any studies comparing past ValueLine dividend growth estimates to actual/future growth rates. It would be interesting to have though!

What I do is to take a look at the 1-year and 3-year growth rates, and use the lowest one. If the rate is very high (eg. 20%) I take even a lower rate. I noticed that this method of approximation seems to be quite close to what ValueLine gives. It is quite a conservative method, however I am not looking for exactly 10% YOC in 10 years (more like 10-15 % in 10 years)

I recently sold CU at around $35 after holding it for about 10 years. I sold it because solar parity is imminent in most of the world (in that the costs of producing solar electricity will be equal to the costs of other forms of production) and because CU uses a lot of coal to generate electricity, which produces a lot of GHGs. This is now a no-no in Alberta and Canada.

While a lot of CU’s operations are likely to be UNaffected by these trends (though how much exactly, I have no idea), some will. The consequence, I think, is that future performance will not replicate past performance.

I would like to know what percentage of CU’s revenue is guaranteed through long-term contracts.

“I have a small spanish dividend growth investment portfolio. I am looking to diversy with international stocks. Which 3 – 5 stocks should you recommend for a long term dividend investment strategy?

Thanks in advance

“

I would stick just with low costs ETFs, other wise just go with banks.