Dividend Growth Investing & Retirement is supported by its readers through donations and affiliate links. If you purchase through a link on my site, I may earn a commission. Thanks! Learn more.

For those new to the blog, I like to keep my readers up to date on portfolio changes. One of the reasons I started this blog was to educate others, but also to improve my own investing. By keeping an open book of my portfolio and changes to it, I hope to generate discussion so others can see how I put my investing philosophy into practice. For the most up to date portfolio changes follow my twitter account as I will usually tweet first and then follow-up with a blog post.

⭐ Find dividend growth stocks that have survived multiple recessions and increased dividends for 5, 10, 25+ years in a row.

On February 23, 2015 I decided to buy Canadian Western Bank (TSE:CWB Trend) again as it had dropped another 10% from my target buy price of $30 to around $27. I picked up shares for an average price of $26.93. I first bought shares in the company on December 16, 2014 at $29.33. With my latest purchase I was able to average down bringing my cost base to $28.45.

Canadian Western Bank is a regional Canadian bank in you guessed it Western Canada (mainly Alberta and BC). They have managed to increase their dividend for 23 consecutive calendar years in a row. They are currently (March 2015) yielding around 3% which is historically high for the company. Their shares are suffering right now because of their exposure to Alberta and its struggling economy with the oil price so low. I took this as an opportunity to buy more shares.

Related article: Canadian Western Bank Dividend Stock Analysis & Portfolio Update

You can see from the chart below that I had an opportunity to buy shares below $27 in late January 2015 and early February, but I didn’t pull the trigger.

At the time the Canadian banks weren’t doing very well and Bank of Nova Scotia (TSE:BNS Trend) had dropped to around $61. I was hoping to initiate a position in Bank of Nova Scotia at $60 so I was waiting for just a bit more of a drop. Rather than invest more in Canadian Western Bank I planned to use the money to add to a new position. Bank of Nova Scotia never dropped to $60, instead increasing in price along with Canadian Western Bank, so in the end I didn’t invest in either at the time. I’d still like to invest in some other Canadian Banks, but they’ll need to fall another 10% or so in price. I already mentioned that I start to get interested at $60 for Bank of Nova Scotia, but National Bank of Canada (TSE:NA Trend) looks enticing too, if drops to $42. The other banks that I’d consider are Toronto Dominion Bank (TSE:TD Trend), Royal Bank of Canada (TSE:RY Trend) and probably Bank of Montreal (TSE:BMO Trend), but they are priced about 20% or more above my target buy price.

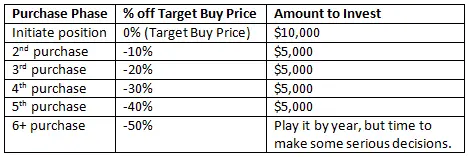

My work-in-progress averaging down plan

When I invest in a company I typically look for a good company that I understand, one with strong financial strength, a long history of earnings and dividend increases, a wide moat, and a sustainable dividend. Once I identify the company, I come up with a reasonably conservative stock price I’d be willing to buy them at. Then I wait, and wait … eventually the price will drop below my target buy price and I’ll have the opportunity to invest. So far this part of my strategy is fairly well planned out. Until recently I didn’t realize that I don’t have an averaging down plan. I have set target buy prices, but I had no defined plan to buy more when the price continues to drop.

I starting thinking about this and came up with a work in progress plan that I’m hoping you’ll comment on. I’ve used the example below with some hypothetical amounts to highlight my plan.

The idea behind this averaging down strategy is that the company fundamentals haven’t changed and I still believe the dividend will grow in a sustainable manner. If this is the case and the price keeps dropping I should be happy to buy more of a great company at even cheaper prices. If the stock gets to 50% below my target price, then I’ll have to make some serious decisions on if I want to make a large purchase to really take advantage.

My averaging down plan is still in the works and I don’t think I’d use it for all my stocks as I’ll have to take into consideration diversification (not being too overweight in one stock or one sector) and risk tolerance. I do like the idea of having a plan in place for stocks that I want to average down with. When people start to panic as prices drop, I want to be able to fall back on a plan that is based on rational thought, not my emotions at the time.

What do you think of this plan and my recent purchase of Canadian Western Bank?

Photo credit: limowreck666 / Foter / CC BY-NC-ND

Newsletter Sign-Up & Bonus

Have you enjoyed our content?

Then subscribe to our newsletter and you'll be emailed more great content from Dividend Growth Investing & Retirement (DGI&R).

BONUS: Subscribe today and you'll be emailed the most recent version of the Canadian Dividend All-Star List (CDASL).

The CDASL is an excel spreadsheet with an abundance of useful dividend screening information on Canadian companies that have increased their dividend for five or more years in a row.

The CDASL is one of the most popular resources that DGI&R offers so don't miss out!

I feel like repeating myself since the beginning of the year, but NA would be my choice among the Canadian Banks right now. I already hold some but would add more without a doubt! It’s a nice small one with a lot of growth potential.

Any plans to average down on ensign serviceS.How you invest, what is thumb rule of percent of trading fee vs Investment.

I averaged down on ensign once already and don’t plan on adding more currently.

I try and keep trading costs to 1% or less. Questrade charges me $5 per trade in general, so my minimum investment would be $1,000. I get charged $5 to buy and then $5 to sell whenever that happens to be. $10 in fees leaves my minimum investment at $1,000 if i want to hit my 1% or less target.

You’re averaging down plan seems to be a dangerous one. You’re trying to catch a falling knife and once and awhile you will get cut. The proper way of averaging down is to use an asset allocation strategy and buy when equities / fixed income and sectors are no longer align according to your long term plan.

I recommend you read a book called: The four pillars of investing.

Good luck

It is a good point about the falling knife.

I don’t plan on using the average down plan if it puts me too overweight in a stock or sector as i want to be within my allocation targets. If I can average down within my allocation limits I want to use an average down plan.

I know, ANALysts…

Here’s RBC’s marketing spiel from this morning fwiw.

Agree with mm comment about falling sharp things. Sometimes you get lucky with good entry but a real challenge to click the buy button if your arms have been previously sliced off.

Do appreciate what you are sharing. Quality stuff.

————————

March 6, 2015

Canadian Western Bank

A bigger “bet” on Alberta, oil and interest rates

Our view: We view CWB’s pivot in strategy as a bigger bet on lending in

Western Canada at a time of elevated risk. We have lowered our target

multiple to 10.0x 2016E EPS from 10.5x to reflect this higher risk. Our price

target falls to $28 from $30. Sector Perform maintained.

Key points:

CWB reported Q1/15 adjusted core cash EPS (on a combined business

basis) of $0.69, below our $0.74 estimate. On a continuing operations

basis, which excludes results from pending business sales, CWB’s cash

EPS was $0.66. We now model CWB on a continuing operations basis and

have updated our historical information to reflect the results of continuing

operations. CWB indicated its recent sales of its insurance business and

trust business for a combined $230 million in cash will increase its Basel

III CET1 ratio by 70 bps.

During the conference call, CWB provided details with respect to the

shift in its longer term strategy and its intent to deploy capital into

lending and wealth management in its core Western Canada franchise.

Particularly, CWB indicated it intends to deploy the capital generated from

recently announced transactions for strategic and accretive opportunities

within faster growing business lines that are better aligned with CWB’s

strategic direction.

In essence, we believe CWB is going “all-in” to pursue core-lending

opportunities in Western Canada despite low oil prices and a potentially

slower Alberta economy. CWB’s management team clearly views the

current environment as ripe for market share gains. While we appreciate

management’s steadfast view that Alberta will not be adversely affected

by low oil prices and that this cyclical low in oil prices should be seen as

an opportunity to seize market share growth by a local bank, we have

reservations. Where CWB sees opportunity we see risk – a risk more

unique to CWB versus other banks we cover.

We have adjusted and updated our earnings model and lowered our

target multiple to reflect, in our view, the higher risk of CWB’s revised

strategy in the context of low oil prices and low interest rates. Our new

target multiple is 10.0x 2016E EPS, which we have lowered to $2.80 from

$2.90. Our price target falls to $28 from $30 previously.

I have added CWB about a week ago at $28.50 and $27. As a fellow shareholder of CWB, I want to say congrats to you and me. It feels great to see you investing in CWB as I always admired your very strong and detailed stock analysis.

Cheers,

BSR

I see you invest 5000$ ..It will take me 5 months to save that amount..What u do if you see market is going down and u dont have enough

The $5,000 used in this post was just an example it isn’t actually how much I invest.

If the market is going down and I don’t have enough money, I won’t invest. It’s hard to pass up an opportunity, but you also don’t want to over extend yourself.

I’m still a fan of the large Canadian banks and have been buying BNS, TD and RY with BMO and CM on my watch list. Thanks for sharing.

I was very close to buying BNS the other week. Price didn’t quite come down enough though.

Hi,

New to investing and have always been interested in dividend paying stocks. Currently have $1500-$2000 to invest. I was considering $500 to invest in 3 or 4 stocks. Areas of interest would be utilities, banks, oil & gas and real estate. Any advice would be greatly appreciated.

Also, what would be a good book to read about retiring and living off your dividends to get a better understanding about this.

Sincerely

DB

You’ll soon be “lucky” enough to buy CWB at $10, then $5, then zero.

You should’ve considered the possibility that this will be a full scale crash, not a buying opportunity.

7 years of rising markets has done what it always does, creates complacent, risk blind investors.

Kiss good bye most of your money.