Dividend Growth Investing & Retirement is supported by its readers through donations and affiliate links. If you purchase through a link on my site, I may earn a commission. Thanks! Learn more.

They say the hardest lessons in life are learned through experience. Well let’s just say a 38.6% loss in about a month is a lot of “experience”.

On November 6, 2015, and December 1, 2015, I purchased shares of a stock that was yielding 8-9% and was guiding annual dividend growth of 6-10% for the next few years. The company had a wide moat and a long dividend streak.

⭐ Find dividend growth stocks that have survived multiple recessions and increased dividends for 5, 10, 25+ years in a row.

Unlike other companies that typically increase their dividend once a year, they’d started increasing dividends every quarter. I got in after the 7th consecutive quarterly dividend increase.

Sounds like every dividend growth investor’s dream, right?

Not so fast …

A week after my 2nd purchase they cut the dividend 75% and I sold the stock; Kinder Morgan Inc. (NYSE:KMI), for a 38.6% loss.

Source: https://ir.kindermorgan.com/dividend-history

Here are the 3rd and 4th lessons I learned in the second part of this 5-part series covering the “8 Lessons I Learned from One of My Worst Dividend Growth Investments” …

You can check out the other lessons here:

- Lesson 1 & 2: Maintaining an “Investment Grade” Credit Rating Matters & Financial Strength Should Never Be Overlooked

- Lesson 5: When the Dividend Yield Gets Really High, It’s A Warning Sign That A Dividend Cut May Be Coming.

- Lesson 6 & 7: Diversification & Asset Allocation Matter & Don’t Forget Income Allocation Too!

- Lesson 8: Know Yourself, Make A Plan and Be Patient

Lesson 3: Don’t Trust Management If the Numbers Don’t Make Sense

Three months before the dividend cut Kinder Morgan was putting on investor presentations like this:

Source: September 10, 2015 Barclays CEO Energy/Power Conference Investor Presentation

Approximately 6% dividend yield and they were planning on 10% annual dividend growth for 5 years from 2015 to 2020.

Two months later, the story from Kinder Morgan changed to 6-10% dividend growth. Lower than the 10%, but still good, especially considering the yield in November was around 8-9% as the stock price had dropped further.

Source: November 18, 2015 RBC MLP Conference Investor Presentation

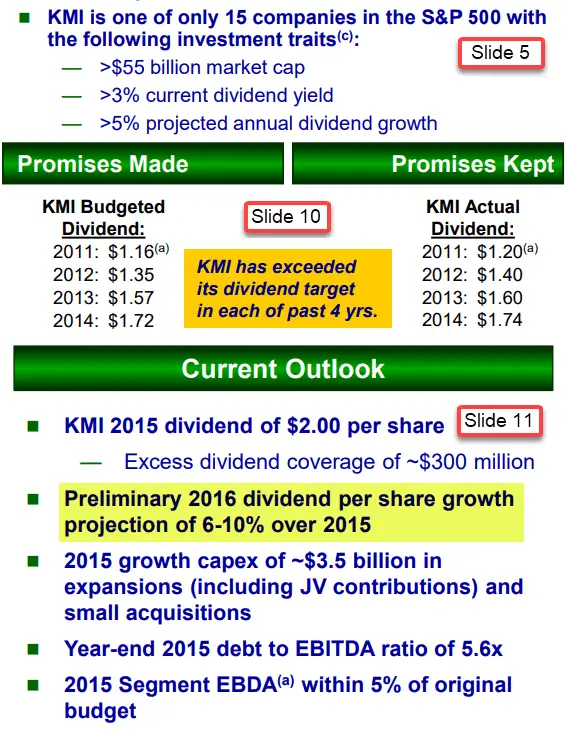

It’s hard to believe that 21 days, just 21 days before a 75% dividend cut; you were seeing comments like these in their investor presentation:

- “Promises Made” “Promise Kept” – “KMI has exceeded its dividend target in each of past 4 yrs.”

- “2016 dividend per share growth projection of 6-10% over 2015”

- “>5% projected annual dividend growth”

The promises made, promises kept slide is almost too good … you know, in a sad, ironic sort of way.

[The dividend cut] “obviously came as a shock to some people, and obviously was deplored by some people”

Rich Kinder, billionaire, and largest shareholder of Kinder Morgan Inc. (NYSE:KMI)

Uh … ya think?

But … I should have known better.

I ignored obvious alarm bells and instead “hoped” they would pay out and grow this very high dividend.

Lesson 4: Never Ignore the Payout Ratio

Don’t rely on what others (management in this case) say when the numbers don’t make sense and never ignore the payout ratio (dividends divided by earnings).

“Dividends are paid from earnings, so you should be sure that dividends are a modest percentage of earnings (this is known as the payout ratio […]). The payout ratio should be less than 60% for nearly all stocks except qualifying utilities, publicly traded partnerships, and Real Estate Investment Trusts. […] In utilities, a moderate payout ratio is under 70%.”

Source: The Single Best Investment: Creating Wealth with Dividend Growth by Lowell Miller (AL):

Kinder Morgan’s payout ratio based on earnings per share was over 100% … well above the 60% that Lowell Miller recommends.

Looking at Kinder Morgan’s December 8, 2015 press release, they would argue that they use distributable cash flow (DCF) “to compare basic cash flows generated by us to the cash dividends we expect to pay out shareholders on an ongoing basis”.

Using cash flow instead of earnings can be made as an argument, but using cash flow instead of earnings is typically riskier.

“Cash flow is notably important in determining the safety of dividends, since it shows you how much is actually available to pay them, though looking at earnings alone is safer, since thatʼs a more conservative number—cash flow is always higher than earnings. However, in the occasional situation in which a dividend payout ratio may be on the high side, if you look to cash flow you may find there are ample resources to cover a dividend, though earnings might look skinny due to high depreciation. This is particularly true of REITs, with their notoriously high real estate depreciation.”

Source: The Single Best Investment: Creating Wealth with Dividend Growth by Lowell Miller (AL, emphasis added)

Kinder Morgan’s payout ratio based on earnings was high (>100%), but even the payout ratio based on DCF was close to 100%. At almost 100%, this wouldn’t qualify as “ample resources to cover a dividend”.

The annual dividend growth of 6-10% that management was forecasting was not sustainable based on these high payout ratios.

You want a lower payout ratio because it leaves the company with more money left over for business growth or a buffer in case something goes wrong … which it did.

On December 1, 2015, in response to Kinder Morgan’s plan to increase their ownership in Natural Gas Pipeline Company of America LLC (NGPL) and add about $1.5 billion in debt, Moody’s changed Kinder Morgan’s credit rating outlook to negative. This was at a time when Kinder Morgan was already at the lowest level of investment grade: Baa3, or the equivalent of BBB-.

A week later, in an effort to maintain its investment-grade credit rating, Kinder Morgan announced a 75% dividend cut.

Because their payout ratio prior to the dividend cut was so high, virtually all spare cash and all of their earnings were going to pay the dividend. They didn’t have enough left over to have the option of using existing cash flows/earnings to pay for the increased ownership in NGPL, so they planned to use debt instead.

Kinder Morgan already had a lot of debt, and taking on more would have dropped their credit rating from investment grade to junk status, so they were forced to cut the dividend instead.

Had the payout ratio been lower and at a more reasonable level, they could have used their existing cash flows/earnings to fund NGPL without needing to cut the dividend.

Ultimately, a high payout ratio was one of the reasons why they cut the dividend.

I went yield chasing towards an enticing 8-9% dividend yield and hoped management would come through on their promise of 6-10% annual dividend growth guidance. Instead, they cut the dividend 75%. By hoping, I ignored obvious red flags like the earnings and cash flow payout ratios which were close to or above 100%.

Had I paid attention to the payout ratio I could have avoided a 38.6% loss and the 75% dividend cut.

Summary

The 3rd and 4th lessons I learned in this 5-part series covering the “8 Lessons I Learned from One of My Worst Dividend Growth Investments” were …

Lesson 3: Don’t Trust Management If the Numbers Don’t Make Sense & Lesson 4: Never Ignore the Payout Ratio

Just 3 weeks before a 75% dividend cut in late 2015; you were seeing comments like these in Kinder Morgan’s investor presentation:

- “Promises Made” “Promise Kept” – “KMI has exceeded its dividend target in each of past 4 yrs.”

- “2016 dividend per share growth projection of 6-10% over 2015”

- “>5% projected annual dividend growth”

And yet, Kinder Morgan’s payout ratio based on earnings was high (>100%), and even the payout ratio based on DCF was close to 100%.

Don’t ignore obvious alarm bells like a high payout ratio and instead hope that management will keep their word.

You want a lower payout ratio (60% or less) because it leaves the company with more money left over for business growth or a buffer in case something goes wrong.

The Other Lessons

They say the hardest lessons in life are learned through experience. A 38.6% loss in about a month is a lot of “experience”, and that means a lot of lessons.

In fact, too many for just one article, so you’ll have to check out the other 4 articles in this 5-part series for the rest of the lessons.

- Lesson 1 & 2: Maintaining an “Investment Grade” Credit Rating Matters & Financial Strength Should Never Be Overlooked

- Lesson 5: When the Dividend Yield Gets Really High, It’s A Warning Sign That A Dividend Cut May Be Coming.

- Lesson 6 & 7: Diversification & Asset Allocation Matter & Don’t Forget Income Allocation Too!

- Lesson 8: Know Yourself, Make A Plan and Be Patient

Newsletter Sign-Up & Bonus

Have you enjoyed our content?

Then subscribe to our newsletter and you'll be emailed more great content from Dividend Growth Investing & Retirement (DGI&R).

BONUS: Subscribe today and you'll be emailed the most recent version of the Canadian Dividend All-Star List (CDASL).

The CDASL is an excel spreadsheet with an abundance of useful dividend screening information on Canadian companies that have increased their dividend for five or more years in a row.

The CDASL is one of the most popular resources that DGI&R offers so don't miss out!

![How to estimate dividend growth and total returns using Josh Peters’ Dividend Drill Return Model [Example & Spreadsheet]](https://dividendgrowthinvestingandretirement.com/wp-content/uploads/2018/10/How-to-estimate-dividend-growth-and-total-returns-using-Josh-Peters’-Dividend-Drill-Return-Model-Cover-768x575.png)

Thanks for another great article and looking forward to the remainder of the series. As a question, would you put Enbridge in the same risk scenario as KMI?

No, I wouldn’t put Enbridge in the same risk scenario as KMI. The 2015 Kinder Morgan had a combination of higher payout ratios and debt than Enbridge currently does. Enbridge has BBB+ credit ratings or equivalent from S&P, Fitch & DBRS. Moody’s is the exception at Baa2. These are better than the 2015 Kinder Morgan had before it cut its dividend.

Enbridge still has its risks, but I don’t consider it as risky as KMI back in 2015 right before the dividend cut.

I had a similar experience with Altagas. I’ve learned the lesson. Don’t chase yield and Debt Doesn’t Disappear even for utilities. I got rid of Inter Pipeline after the recent run up, I’m too nervous for these kind of high yielders now. I prefer not to be faked out by current yield and focus on dividend growth instead.

Super Newbie needs some help here. I looked up DPR and found it to be =Div/Net income. I use Yahoo finance to find my numbers. I’m obviously not using the correct numbers as for enbridge I’m getting a payout ratio of 153% instead of 65%. The numbers I used are Net income applicable to Common Shares 251500 (in income Statement) and 3844000 for Dividends (in cash flow) both under the Financials heading. What numbers should I be using? Thanks

You can calculate a payout ratio using different methods. You used earnings/net income and got a payout ratio of 153% which sounds about right for Enbridge.

If you use distributable cash flow (DCF) you’ll get around 65% (Dividends per share / DCF per share). Using DCF to calculate a payout ratio is a less conservative method than earnings, but one that some pipeline companies use.

Excellent comments on Enbridge. How can companies continue paying a div for yrs that exceeds their earnings? It appears that some will borrow using LOC or is it simply that considering their cash flow (depreciation expense etc that is not really cash leaving the co.) they have enough to pay the div with probably very little more? Neither situation would be good (using debt or having very blittle cash flow other than to pay the div)?