Dividend Growth Investing & Retirement is supported by its readers through donations and affiliate links. If you purchase through a link on my site, I may earn a commission. Thanks! Learn more.

Before I go into my dividend stock analysis of Shaw Communications I’d like to mention another important article that can be used in conjunction with my dividend stock analyses. To get an understanding of why I look at various measures and what I’m looking for in a company read Deciding Which Stocks To Buy: Dividend Growth Investing Criteria first. And now onto Shaw Communications…

Company Description

⭐ Find dividend growth stocks that have survived multiple recessions and increased dividends for 5, 10, 25+ years in a row.

Here is the business summary from Yahoo Finance:

Shaw Communications Inc. provides broadband cable television, Internet, home phone, telecommunication, and satellite direct-to-home services in Canada and the United States. It offers cable television services, such as on demand programming comprising pay-per-view and video-on-demand services; digital programming; high definition (HD) television, including three dimensional HD; and Internet access services. The company also provides digital phone services, such as long distance and calling features; and managed and hosted PBX, and primary rate interface services. In addition, it develops and manages fiber network that carries digital phone capacity and video signals, as well as provides services to small and medium size businesses, Internet service providers, cable companies, broadcasters, governments, and other organizations that require end-to-end Internet, data, and voice connectivity. Further, the company owns and leases satellite transponders that receive and amplify digital signals and transmit them to receiving dishes; distributes digital video and audio signals through satellite infrastructure; and offers digital video and audio programming services from satellites directly to subscribers homes and businesses. Additionally, it provides uplink and network management services to conventional and specialty broadcasters; and asset tracking and communication services to the transportation industry, as well as redistributes television and radio signals through satellite to cable operators and other multi-channel system operators. The company primarily serves residential and business customers. As of August 31, 2012, it served approximately 2.2 million cable television and 1.9 million Internet customers, as well as 1.4 million digital phone lines. The company was formerly known as Capital Cable Television Co. Ltd. and changed its name to Shaw Communications Inc. in May 1993. Shaw Communications Inc. was founded in 1966 and is based in Calgary, Canada.

10 Year Stock Chart

Looking at the 10 year stock chart, there is a 10 year annual average return of 10.2%. If we include the dividend payments over the past 10 fiscal years (Total dividends paid of $5.19) then the total average annual return would be 12.5% with the average return from dividends representing 2.3%.

Most of the significant gains came from 2003 to the end of 2007. Since then the price has fluctuated between the high teens and mid twenties. Whenever I look at a 10 year stock chart I expect to see a big drop around March 2009 because of the global financial crisis. With Shaw Communications there isn’t a noticeable drop in 2009, and seems to have weathered the storm fairly well.

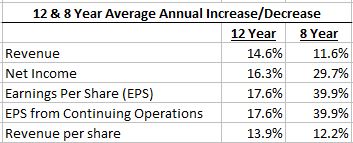

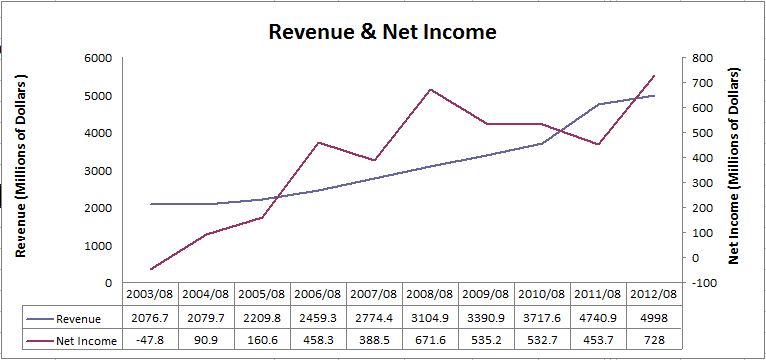

Revenue & Earnings

From fiscal 2001 to 2003 Shaw Communications had negative earnings, so I’ve shown the 12 and 8 year averages instead of the 10 year average.

The 12 and 8 year averages show a strong ability to grow both revenue and earnings. I like to see 8% or higher in all categories, which Shaw has been able to do. The three years of negative earnings from fiscal 2001 to 2003 takes some of the pristine out of these numbers, but all-in-all these are impressive numbers.

Revenue and net income show a nice trend up, however when you look at net income it starts from a negative number in 2003. The company hasn’t lost money since then, and has grown net income considerably. The upward trend in this chart is appealing, however when the same ratios are examined on a per share basis it shows a much more erratic story.

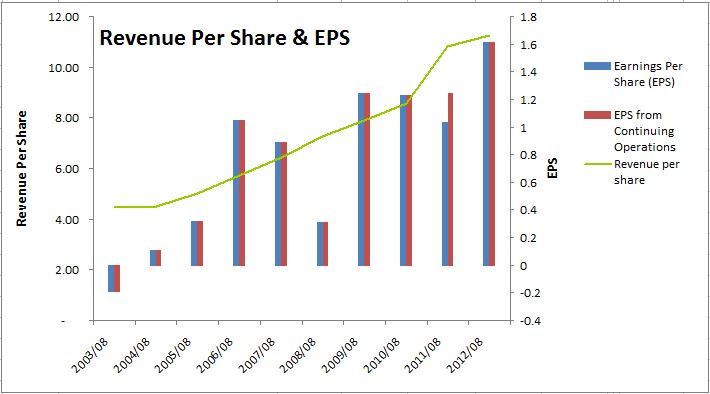

You can see from the above chart that EPS has fluctuated quite a bit over the past 10 years. Revenue per share shows a nice upward trend and has grown at a good rate, but I’d prefer to see a steadily increasing EPS to match the revenue.

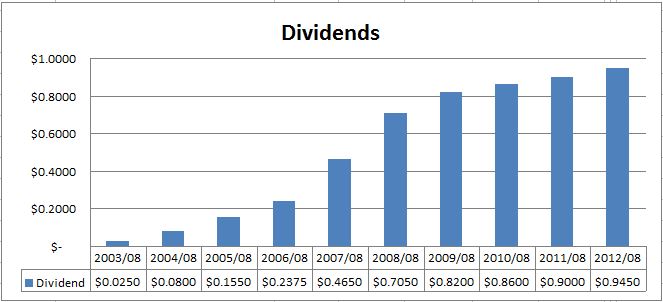

Dividends

A quick look at the Canadian Dividend All-Star List tells me that Shaw Communications has increased their dividend for 10 consecutive calendar years in a row. For a Canadian company this is an impressive streak. If Shaw can continue to pay out its dividend for the remainder of the year; which I expect them to, then this will mark 11 consecutive years of increasing dividends.

Dividends have been steadily increasing over the years which is a good sign, but it looks like the significant dividend growth occurred from 2003 to 2008, with the past 4 or 5 years showing a slowdown in dividend growth.

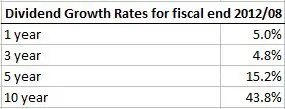

Dividend Growth

The most recent monthly dividend increase happened with the dividend recorded in March 2013. The monthly dividend increased by 5.2% from $0.0808 to $0.0850. The latest increase is what I’d expect as you can see that more recent dividend growth rates are around 5%.

The 5 and especially the 10 year growth rates are high, and both above the 8% rates I like to see. The dividend growth rates have slowed in the past few years, and I’d like to see them get back over 8% if they can be paid out in a sustainable manner. I’ve said before that past dividend growth rates can be used to predict future rates, but the 10 year rate is very high and a similar rate going forward would not be sustainable. When EPS growth is compared to dividend growth you can see that dividends have been growing at much faster rate than EPS.

I’ve shown the 12 year growth rate instead of the 10 year rate because of the negative EPS in fiscal 2001 to 2003. As you can see dividend growth has been about double that of EPS, which is not a sustainable trend.

Dividend Sustainability

To get a better idea of the dividend growth going forward the past payout ratio and estimated future earnings should be examined.

- Payout Ratio

Shaw Communications payout ratio at the end of the most recent fiscal year end was 58.7%. For most companies a payout ratio of 60% or less is good, but some industries like the cable/telecom industry typically have higher payout ratios (60-80%). This indicates that Shaw still has some room to grow it’s dividend.

If we look at the chart we can see that the payout ratio for the past 5 years is usually around 60% to 70%, with the exception of 2008 when it spiked up. I expect Shaw Communications to try and maintain a similar level (60-70%) going forward.

- Estimated Future Earnings

Analysts are currently estimating that Shaw Communications will grow it’s EPS at 5.97% annually for the next 5 years. It’s best to take these estimates with a grain of salt as a lot can happen in 5 years, and the further away the estimate the less accurate it gets. That said, analyst estimates can still be useful when trying to guess future dividend growth rates (The key word being guess).

Based on Shaw’s previous payout ratios and the estimated future earnings I’d expect Shaw to continue to raise its dividend annually at a rate around 6.4% to 9.8%. Based on the past few years of dividend growth at around 5% I’d expect the dividend growth to be at the lower end of the 6.4% to 9.8%.

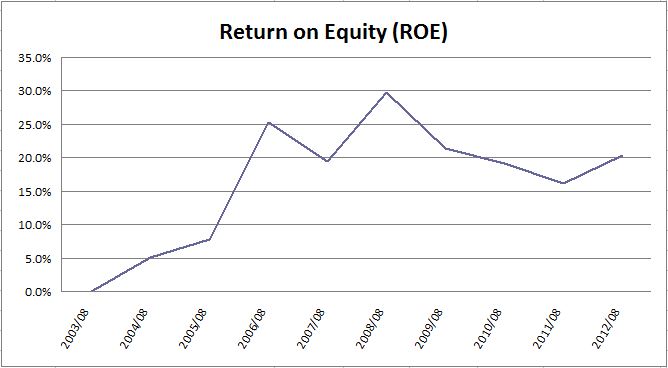

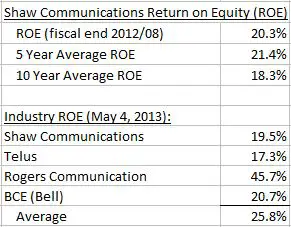

Competitive Advantage & Return on Equity (ROE)

Shaw Communication does most of its business in Western Canada where its main competitor is Telus. There is a worry that Telus will steal market share over the next few years, and I think this is a valid concern as Shaw has been losing customers to them already. While this is a concern, there isn’t a whole lot of choice in Canada for cable or internet services, which in itself is a competitive advantage. The chart below show’s a strong ROE of around 20%.

Fiscal 2003 to 2005 are low, but for the past 7 years Shaw has been able to keep ROE at or around 20% which is good. Let’s see how well this stacks up against its competitors. In Canada I’d say there are 3 other main companies that compete with Shaw: Telus, Rogers Communications, and BCE.

Shaw’s main competitor is Telus and it currently has a slightly higher ROE which is a good sign. Shaw is under the average, but this is largely due to Roger Communications impressive ROE of 45.7%. Shaw Communication’s ROE is in-line with industry averages and it’s only slightly under BCE’s ROE of 20.7%. Because Shaw operates in an industry without a lot of competitors it has some competitive advantage. This advantage is lessened because it’s competitors are large highly competitive companies. I would say that overall they do not have a sustained competitive advantage.

Debt & Liquidity

Normally I like to see a current and quick ratio above 1.0 and a debt to equity ratio less than 1.0. In this industry it is typical for companies to take on more debt however. If we look at the 10 year history we can see that debt levels are roughly in line with the past.

![]()

Overall I would say that debt levels are OK, but not great.

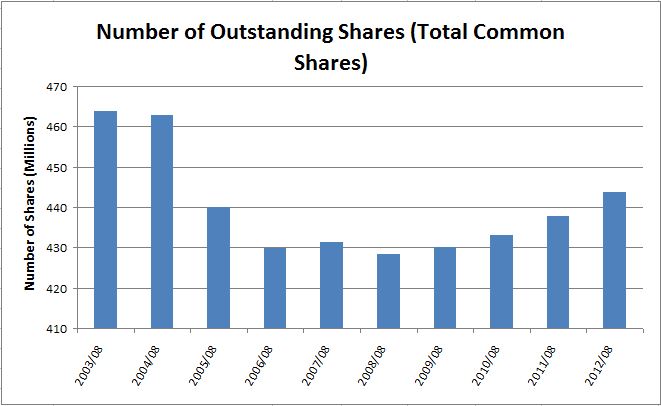

Shares Outstanding

Shares have decreased from 10 years ago, however they have been steadily increasing over the past 5 years.

I don’t place a lot of importance on shares outstanding, but if there is a trend I’d rather see it go down or stay roughly the same. With Shaw there is an upward trend for the past 5 years.

Valuation

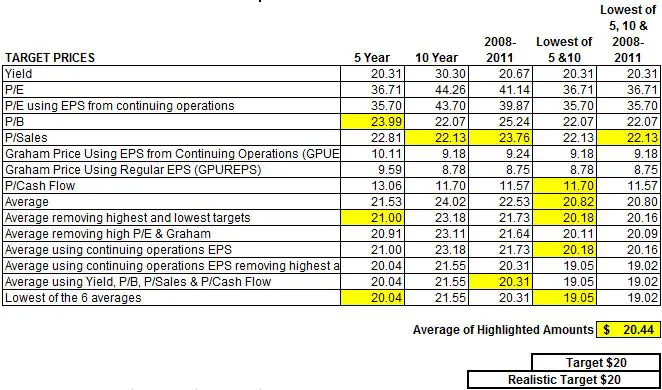

I use 6 main ratios to determine a fair price: Yield, Discount/Premium of the low price compared to the Graham Price, P/E, P/B, P/Sales and P/Cash flow. I like to look at both EPS and EPS from continuing operations so it ends up being a total of 8 ratios as the Graham Price an P/E both use EPS.

I use the lowest price for the fiscal years to determine the 5 year, 10 year and 2008-2011 averages. Investors commonly use 5 and 10 year averages, but I like to include the fiscal 2008 to 2011 low price average, as I feel that the low prices during this era represent a reasonably low stock price. During 2008 and 2009 most companies experienced a really low price due to the Global Financial Crisis followed by increases in 2010 and 2011.

I get the following for Shaw Communications.

* Calculation Notes: I compare the low price to the calculated Graham Price (GP) to determine the discount or premium to GP. I calculate the GP using the square root of (22.5 x Book Value x EPS*). For EPS in this formula I use the lesser of the 3 year EPS average or the current EPS. If the GP calculated is negative then I set the Discount/Premium to GP as -25%. The other ratios are calculated in the normal fashion.

The majority of my valuation methods use historical averages, so it is important that you expect the company to continue to operate in a similar manner to its past. If you expect the company to change, these valuations become less useful.

Now that I have these different averages, I can use them to determine a target price. Using these averages will create a lot of different target prices, so I like to compare this strategy to previous years. Ideally what I’m looking for is a strategy that would have given me a chance to buy the stock in two to three fiscal years in the past 10 fiscal years. It’s not always possible to test my strategy back 10 years, due to limited financial information, but I do my best.

In the below table I was able to highlight the target prices from strategies that would have given you a target price above the low price in 2 – 3 of the past 10 fiscal years. I’ve used the average of these to determine the target price of $20.

I would say that this strategy is quite conservative and as a result I don’t buy stocks very often. I’m usually waiting around for a few months before I’m able to buy something from my dividend watch-list. This is fine by me as I’m young, so I’ve got the time and it pays to be patient. Sometimes my target price is too conservative. So much so, that occasionally I have to revise my target up. I like to use the yield as a way to gauge if my targets are realistic or not. For instance if my target price would result in a dividend yield that has never been paid by the company, then odds are the price isn’t going to come down that low. In these cases I adjust my target to a more realistic value. In rare instances I’ll adjust my target down further. With a current monthly dividend of $0.085 the yield on $20 would be 5.10%. This is in line with the highest yields during the past 5 years, so I’ve kept the realistic target the same as the original.

Before I buy a stock I like to look at Morningstar’s 5 star rating as a quick way of seeing what others think of the stock. If a stock has a 4 or 5 star rating then they consider the stock to be trading at discount to fair value. A 1 or 2 star rating indicates a premium to fair value and a 3 out of 5 rating suggests the price is close to fair value. Shaw is currently around $23, and Morningstar rates it 3 out of 5 stars.

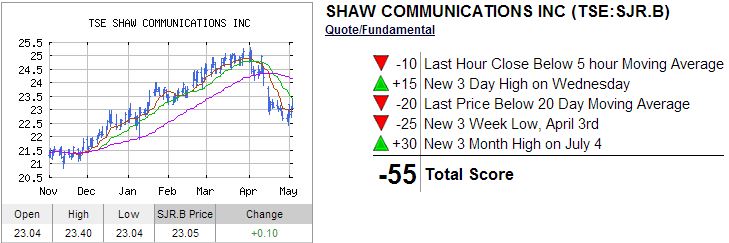

Trend Analysis

I also like to look at INO`s Free Trend Analysis prior to investing to see if I should hold off or not. Sometimes it is nice to see if the stock is trending down or up before buying it. INO currently shows the following:

To see the most recent trend analysis for Shaw Communications click here. INO also has a list of the top 50 trending stocks and free trading seminars and videos.

Conclusion:

Overall Shaw shows some compelling numbers when looking from a 10 year perspective, but more recently the company has seen a loss of customers to their main competitor Telus and their 5 year history isn’t as compelling. Their dividend growth has been great and I expect future dividend growth to be in the range of 6.4% to 9.8%, likely on the lower end of this range. Shaw has shown a good ability to grow revenue and earnings while maintaining a respectable ROE of around 20%, but in light of increased competition from Telus it remains to be seen if they can keep this up. Whether I’d invest in this company was a difficult decision for me to make, but I’ve decided I would invest in this company should the price come down below my target price of $20. If you look at the 10 year chart you can see that over the past 5 years the price has come down to around $18 or $19 at one point or another each year, so you may even want to try for a slightly lower price than my $20 target.

Disclaimer

I am a blogger and not a financial expert. These writings are my own opinions and should not be considered financial advice. Always perform your own due diligence before purchasing a stock. I mention target prices in this article, but this is not a recommendation to buy this stock, it is just a target price I use for my own personal investing that I have chosen to share.

Newsletter Sign-Up & Bonus

Have you enjoyed our content?

Then subscribe to our newsletter and you'll be emailed more great content from Dividend Growth Investing & Retirement (DGI&R).

BONUS: Subscribe today and you'll be emailed the most recent version of the Canadian Dividend All-Star List (CDASL).

The CDASL is an excel spreadsheet with an abundance of useful dividend screening information on Canadian companies that have increased their dividend for five or more years in a row.

The CDASL is one of the most popular resources that DGI&R offers so don't miss out!