Dividend Growth Investing & Retirement is supported by its readers through donations and affiliate links. If you purchase through a link on my site, I may earn a commission. Thanks! Learn more.

McDonald’s [MCD Trend] has been on my personal watch-list for quite a while now, but the price hasn’t come very close to my target buy price of $88 so it fell off my radar a bit. The other day I read an article in the Globe & Mail called “McDonald’s stock may yet regain its sizzle” by John Heinzl that sparked my interest. When I read his article it reminded me that McDonald’s is due for a dividend increase in about 2-3 weeks time, so it might be time to increase my target buy price and have another look at McDonald’s.

⭐ Find dividend growth stocks that have survived multiple recessions and increased dividends for 5, 10, 25+ years in a row.

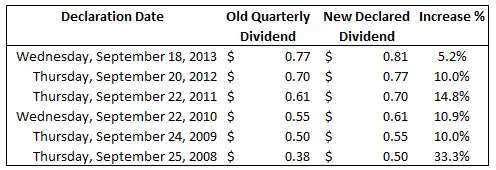

My target buy prices are based on a number of different factors, but I usually use dividend yield to tweak them to a reasonably conservative target. McDonald’s has been increasing its dividend for 38 years in a row, and in the past decade they’ve declared annual dividend increases in mid to late September. I’d wager this trend will continue. Here’s a look at the past 6 dividend increases:

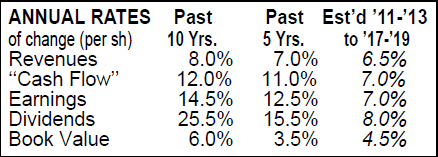

McDonald’s is an internationally known restaurant chain that sells fast food across the world. This wide moat company has 5 and 10 year dividend growth rates of 13.9%1 and 22.8%1, and offers a dividend yield of 3.46% at the August 29, 2014 closing price of 93.72. Based on these numbers it is easy to understand why I’d be interested in this stock. While the 5 and 10 year dividend growth rates are impressive, they have been fuelled by an increasing payout ratio, as dividend growth has exceeded earnings growth over the past decade.

In 2004 the payout ratio was 28%2 and it is currently sitting around 60%2. I don’t expect McDonald’s to go too much above a 60% payout ratio, so future dividend growth will likely be limited to their earnings growth.

Over the next 3 to 5 years Valueline currently estimates annual growth rates of 7.0%2 and 8.0%2 for earnings and dividends. These rates; while not as high as prior years, are still good.

Yahoo! Finance has the annual earnings growth estimates at 6.16%3 for the next five years, which is around Valueline’s estimate. Based on these estimates I think it’s fair to say that over the next 5 years you could expect an average annual dividend growth rate around 6% to 10%, with my best guess likely somewhere in the middle around 8%. Trying to estimate dividend growth for 5 years accurately is a bit of a fool’s errand, but I like to go through the motions, to at least see that the 8% dividend growth I target in my holdings is at least likely. This lets me weed out no or low dividend growth stocks that don’t fit my investing philosophy.

McDonald’s September 2014 Expected Dividend Increase

John Heinzel mentioned in his “McDonald’s stock may yet regain its sizzle” article that “Bloomberg estimates that the next increase will be about 13 per cent.” McDonald’s has been going through some troubles lately with same-store sales flat or declining slightly. This coupled with the Chinese food safety concerns, the recent Russian stores closures, and the payout ratio hovering around 60% make me hesitant to expect a 13% dividend increase. While it’d be a nice surprise, I used a more conservative 5% dividend increase to tweak my target buy price from $88 to $93 ($88 x 1.05 = $92.40 rounded up to $93).

Valueline is estimating that in 2014 they will declare $3.282 in dividends. With 3 dividends already declared this year at $0.81 per quarter, it would appear they are estimating a 4.9% increase to $0.85 [3.28 – ($0.81 x 3)] per quarter.

Looking at David Fish’s US Dividend Champions list I can see that since 2000 the three lowest year over year dividend increases were 4.4%, 4.7% and 8.3%.

Between this table and the Valueline estimate I feel that a 5% dividend increase is a realistic increase to expect, with room to be pleasantly surprised. Past results can’t predict the future, but when it comes to dividends they can tilt the odds in your favor. Based on these factors I’m comfortable increasing my target buy price to $93 before the dividend increase is announced.

Related article: Can Past Dividend Growth Rates Be Relied Upon To Predict Future Rates?

Why I bought shares

I bought shares on August 28, 2014 for an average price of $93.96 (trading fee included) in my taxable account. On September 5, 2014 I purchased some more shares in my RRSP with a bit of US money that was left in the account for an average price of $93.11. These are above my target price, but only slightly (~1%). I’m using the Smith Maneuver now which means I’m moving money from my line of credit to my broker account and logistically I’d rather be buying shares right away with this money so that the audit trail is clear. In the end, rather than waiting for the price to drop a bit more I chose to just buy the shares as I was eager to own a dividend growth stock of McDonald’s caliber.

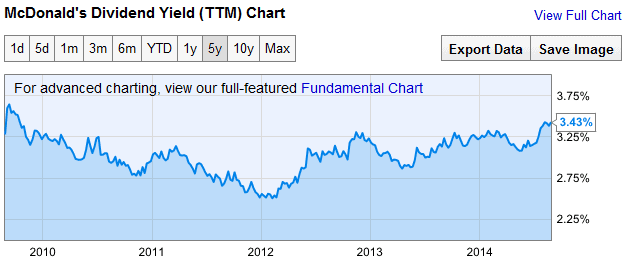

Another important reason is obviously the price. Looking at the August 29, 2014 trailing twelve month (TTM) dividend yield chart below you can see that dividend yield is as high as it’s been since late 2009. This is a good indication that the share price is reasonably cheap, and with a dividend increase expected shortly the yield could be going even higher if the price stays the same.

I’ll get around to completing a full dividend stock analysis eventually, but in the meantime here are the bullets of why I bought these shares.

- Wide moat stock

- Long dividend streak of 38 years

- Dividend is sustainable (Payout ratio is around 60%)

- I expect long term dividend growth around 8%

- Strong financial strength (Valueline currently rates them A++2)

- Dividend yield is high for McDonald’s (Above 3.4%)

- They have consistently increased earnings year after year for the past decade.

- Current short term problems have brought the share price down to a reasonable price. I expect McDonald’s to rebound in the long term.

Conclusion

I get nervous buying in a market that has been going up for so long and seems to reach new highs every other day. When I hear words like “correction” thrown around I find it harder to buy shares, but I still do. For me it’s about the individual company not the market. In McDonald’s case the share price has actually come down over the past year and if there is a further significant drop in McDonald’s, then I’d likely just buy more shares.

I have to remind myself that I’m looking for great dividend growth companies with reasonably cheap valuations, not investing in the whole market. To find these companies at reasonable prices it often means buying during some short term crisis/problem that has spooked investors. In these situations a certain amount of nervousness is expected. With great companies opportunities like these don’t come around very often, which is why I decided to pull the trigger and buy McDonald’s.

Footnotes/Sources:

1 7/31/2014 version of David Fish’s US Dividend Champions excel file. Link: http://dripinvesting.org/tools/tools.asp

2 August 29, 2014 ValueLine Summary of McDonald’s. Link: http://www3.valueline.com/dow30/f5707.pdf

3 Yahoo! Finance Analyst Estimates Page on August 29, 2014. Link: https://ca.finance.yahoo.com/q/ae?s=MCD

Photo credit: http://www.freedigitalphotos.net/

Newsletter Sign-Up & Bonus

Have you enjoyed our content?

Then subscribe to our newsletter and you'll be emailed more great content from Dividend Growth Investing & Retirement (DGI&R).

BONUS: Subscribe today and you'll be emailed the most recent version of the Canadian Dividend All-Star List (CDASL).

The CDASL is an excel spreadsheet with an abundance of useful dividend screening information on Canadian companies that have increased their dividend for five or more years in a row.

The CDASL is one of the most popular resources that DGI&R offers so don't miss out!

Thanks, I really appreciate you sharing what you’re buying, and why, stock by stock to get back in the market.

I’ll be following closely as I also have a lot of cash on the sidelines. And I’m a fellow Canadian so will be very interested in what Canadian companies you choose.

Ps. do you follow Stockchase? A website that compiles comments and recommendations from Canadian experts when they are on Business News Network (BNN). Canada’s business and financial news television channel.

I don’t follow stockchase, but I had a look and it looks like it could be a useful starting point for researching a company.

You spend a lot of time looking at the financials but not at the business itself.

I am also interested in McDonald’s but am concerned about their menu which is getting old and dated.

Young people may have been raised on Mickey D’s but they’re not eating there like their boomer parents did.

McDonald’s has a very fast service strategy, they have a strong breakfast segment (their coffee is very good), great real estate and other pluses. But their menu is just plain old. I might jump in too next week but I have concerns.

Definitely valid concerns about the menu and millennials. I read a few other articles as research and this seems to be a common worry, but in the long term I think McDonald’s will figure it out. It might be a bumpy ride along the way, but they’ve been doing this for a long time, so long term I think they’ll figure it out and transition to a better menu.

There are always going to be business problems that need to be solved in any company, so for me it comes down to how well they are managed. Do they have the people in place to solve problems? Morningstar currently rates their Stewardship Rating as Exemplary and I would agree that overall McDonald’s is a well-managed company, so while the menu and shifting food trends are a big issue I think management will be able to handle these problems.

I have MCD on my watchlist. What’s held me back from jumping in is their slowdown in dividend increases beginning in 2011. If they go back to a double digit increase in their announcement, expected later this month, I’m in.

If they announce a double digit increase and the price stays around $93 or lower, then I will consider doubling up my investment.

MCD hasn’t been doing too well lately but I think that means it’s a great time to buy some MCD shares.

Good analysis work. MCD is definitely having a great sale. Not as great as from 1999-2002, but still good. I haven’t started my dividend growth portfolio yet…I’m still focused on capital growth. But it sure does look good for a long term dividend portfolio. The only thing that worries me about MCD being down is what it means for the overall economy. MCD is one of those companies that does well during recessions, but with it being down I’m wondering i we have some stormy weather ahead.

Hi,

Great minds think alike! I doubled my investment in MCD recently.

Keep your great work. I like your stock analysis.

My big problem with McDonalds is it is a US stock. The big problem with that is you always loose points doing the conversion and then back again when you sell (if you don’t keep the funds in US dollars). Almost feels like a mutual fund. The worst part is not knowing long term what will happen to the US dollar. My father’s only real mistake in 30 years of dividend investing was buying US companies. A lot of them were purchased when the dollar was in the .70 range. Years later when the CAN$ went above the US$ a significant proportion of the gains were wiped out. I think for a long term purchase that needs to be a consideration and with the experiments they are doing with quantitative easing it is a concern.

Tom,

I only think of my US stocks on an income perspective as they’re buy & hold for me. The lower our $Cdn gets the higher the dividend is. There’s also far more choices for great dividend growth stocks south of the border. If you hold a US dividend growth stock for a long time the currency differential on the purchase price becomes very insignificant.

Hey Bernie

I agree with all your points except for the case where the Canadian dollar is not falling relative to the US dollar. Against the headwind of the Canadian dollar gaining 40% on the US dollar as it did in my father’s case the dividends shrank and the capital gain paltry when it was time to sell the investment. With the US actively trying to devalue their currency to boost exports and make their debt more affordable it is still a risk that is on the table. It is much like real estate. Can be a great investment when values are increasing. There is not doubt there are some spectacular companies to invest in down there.

Tom

Tom,

The $CAD has been falling in relation to the $USD since early Sep 2012. It peaked then at $1.0359 & closed today at $0.9019. Many are forecasting it to get to $0.85 before levelling off.

First, I would like to thank you for your time and effort in you great website and analysis. I am new to the game and was wondering if you would recommend a discount broker? I read that you use Questrade and TD… I am torn between Scotia iTrade as it is my bank and Questrade. I don’t have a lot of money just looking to start my portfolio with some DRIPS and a few long postions in the states… I heard good and bad things about Questrade like low fees but bad customer service and start up time… Any tips or thoughts would be appreciated.

The start up time wasn’t bad for me with Questrade and I’ve had mixed results with customer service. I really like being able to online chat with customer service instead of waiting on hold on the phone. Overall you’ve summed it up pretty good: Low fees, not the best service. My experience with brokers in general or banks for that matter is that overall I’m not impressed with the level of service I receive.

What kind of DRIPs do you plan to use? If you are planning on DRIPing in a broker account than Questrade is OK, but not the best because they don’t match the DRIP discount if they offer one. If you are opening traditional DRIPs with a transfer agent, then Questrade is a bad choice because they charge very high fees for certificate deposits and DRS transfers.

Brad,

http://www.moneysense.ca/invest/canadas-best-discount-brokerages-2014

http://www.milliondollarjourney.com/review-canadian-discount-brokerages.htm

http://www.dripprimer.ca/canadiandiscountbrokers

Random question, do you just invest the American dividend companies into your RRSP? Just asking because I know it is more beneficial (tax wise) to invest in Canadian companies. But a lot of the companies I like are American but I know I’ll be taxed higher… which is frustrating.

You can see my portfolio here which separates my investments by account (Taxable, TFSA, RRSP).

Cheers,

DGI&R

Andrew,

I’m not fond of withholding taxes so I place foreign stocks in my RRSP. I know you can claim the withholding taxes as a deduction at tax time if you trade foreign stocks in your non-registered account but it’s just less hassle for me to hold Cdn only there.