Dividend Growth Investing & Retirement is supported by its readers through donations and affiliate links. If you purchase through a link on my site, I may earn a commission. Thanks! Learn more.

In this article, we’ll review all utilities in Canada that have increased their dividend for 5 or more years in a row and apply a dividend growth screen to try and find the best high-quality utility companies for further consideration. Turns out there was only one company that passed all of the criteria, but there are still a few other companies that are worthy of your consideration.

⭐ Find dividend growth stocks that have survived multiple recessions and increased dividends for 5, 10, 25+ years in a row.

Why utility companies make good dividend growth stocks

Utility companies typically have a high dividend yield and make good dividend growth candidates because they operate in a regulatory environment which limits competition and keeps earnings relatively predictable.

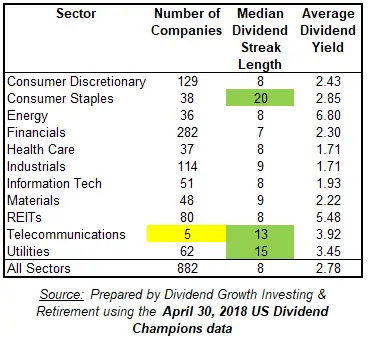

You can see from the table below that the utility sector is one of the of three sectors with typically long dividend streaks, but it also provides a high average dividend yield.

Please note that the table is based on data from the US Dividend Champions list and is limited to the 882 companies that have increased their dividend for 5 or more years in a row. The Canadian Dividend All-Star List in comparison only has around 100 companies which was not enough data to create a meaningful table.

A long dividend streak and high dividend yields aren’t the only criteria we should be looking for though. As Lowell Miller so aptly put it:

Source: The Single Best Investment: Creating Wealth with Dividend Growth by Lowell Miller (Affiliate link, but I personally own and highly recommend this book.)

A long dividend streak is one sign of a high quality, but it is also very important to look at the financial strength of the company too. Utilities typically have a high current dividend yield, but they are more known for low to moderate dividend growth. That’s why it’s important to try and identify the higher growth companies in this sector.

Utility Dividend Growth Screen

I used the following requirements:

Dividend Metrics:

- Used the April 30, 2018 version of the Canadian Dividend All-Star List to find all utility stocks with a dividend streak of 5 or more years.

- A high dividend yield of 4% or higher.

- Estimated future dividend growth of 6% or more. I used Value Line’s estimated annual dividend growth rates for the next 3-5 years for my estimates. Where Value Line wasn’t available I used Tomson Reuter’s analyst estimates which forecast to Fiscal Year (FY) 2020, 2021 or 2022.

- A reasonable payout ratio of 70% or less based on the next 12 months EPS estimates (Dividend / N12 EPS).

- Two of the utility companies in the list are Limited Partnerships which use funds from operations (FFO) instead of EPS to assess their performance so I also included a reasonable payout ratio of 70% or less based on the FY 2018 FFO estimate.

Quality Metrics:

- Value Line financial strength of B+ or better.

- S&P credit rating of BBB or higher.

- Moody’s credit rating of Baa2 or higher.

- DBRS credit rating of BBB or higher.

Normally I’d add in a Morningstar moat rating of narrow or wide as another quality metric requirement, but Morningstar only rates 2 out of the 8 Canadian utilities so I didn’t use it this time. That said, most utility companies with dividend streaks of 5 or more years are rated as narrow.

When I reviewed the 62 US utilities with a dividend streak of 5 or more years Morningstar covered 30 of them. Of the 30 companies, there was 1 wide moat, 24 narrow moats, and 5 with no moat. As you can see the vast majority of utility companies are considered narrow-moat companies.

The Results

Hopefully one of the below data sources will work for you :).

- Your best bet for the data is a sortable excel spreadsheet available here.

- I’ve also made the same data available as a Google spreadsheet here (Also embedded below).

So out of the 8 utility stocks in the Canadian Dividend All-Star List, only one passed all of my dividend and quality metrics screen, but there were a number of close calls that could also be of interest. I’ve broken out the results into three categories: “The Winner”, “Close Calls”, and “Losers”

The Winner:

- Canadian Utilities Limited (TSE:CU)

Close Calls:

- Fortis Inc. (TSE:FTS; NYSE:FTS)

- Atco Ltd. (TSE:ACO-X)

- Brookfield Infrastructure Partners LP (TSE:BIP-UN; NYSE: BIP)

- Emera Inc. (TSE:EMA)

- Algonquin Power & Utilities Corp. (TSE:AQN; NYSE:AQN)

Losers:

- Brookfield Renewable Energy Partners LP (TSE:BEP-UN; NYSE:BEP)

- TransAlta Renewables Inc (TSE:RNW)

Let’s start by looking into the winner a bit more and then I’ll briefly discuss the other companies.

The Winner

Canadian Utilities Limited

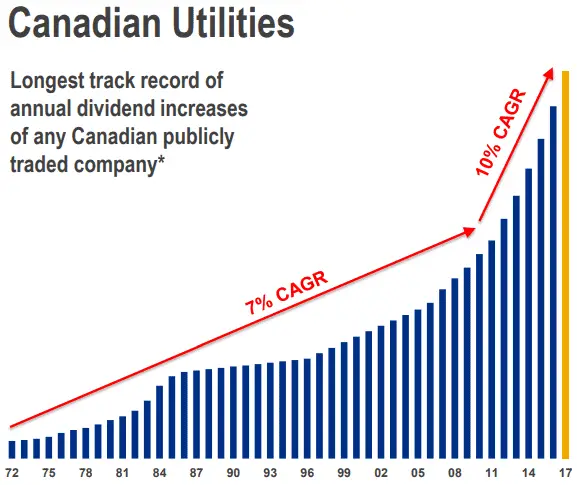

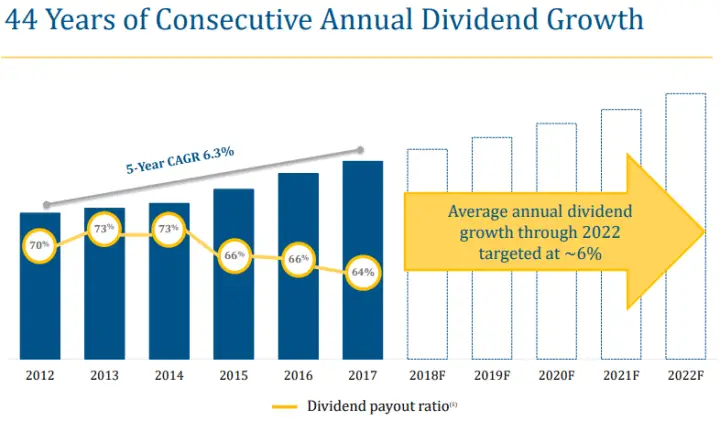

Canadian Utilities Limited is a diversified utility that has two main business units: Pipelines & Liquids and Electricity. Almost all of its earnings are regulated and it has the longest dividend streak (46 years) of any company listed on the Toronto Stock Exchange. What sets this company apart from most of the other utility companies in Canada is that it passed all the criteria, but still has a higher credit rating than most of the other companies in the list. S&P rates them an A- and DBRS givens them an A.

Source: Canadian Utilities Limited “Investor Overview” webpage

From a dividend growth standpoint, there is a lot to like about the company. It has a 5 and 10-year dividend growth rates of 10.1% and 8.6%. It appears that strong dividend growth can be expected to continue as their most recent dividend increase was 10% and analysts are estimating 6.3% dividend growth from fiscal year (FY) 2018 to FY 2022.

Source: February 2018 BMO Infrastructure & Utilities Conference Presentation

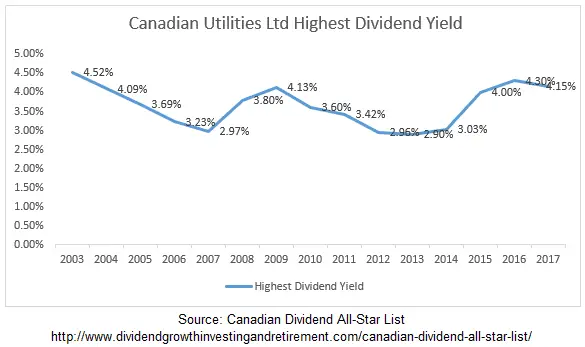

It is also currently yielding 5.1%, which historically is very high for the company. In fact, it hasn’t been this high in over a decade.

All-in-all I’m a big fan of Canadian Utilities which is why I bought shares back in 2015 at $30 per share and more recently I added to my position at $32.90. I’ve also got an open order for more at $28 should the price drop further. At $33 or under I think Canadian Utilities offers good value.

Close Calls:

Fortis Inc.

Why it failed: Moody’s credit rating was Baa3 when Baa2 or higher was needed.

Despite the failing credit rating from Moody’s they still passed the S&P and DBRS credit ratings. S&P gave them an A-, but with a negative outlook and DBRS was BBB (high). The average rating of all three rating agencies would be around BBB to BBB+, so overall, I think Fortis is still worth your consideration.

Source: April 2018 Investor Relations Presentation

As you can see Fortis has an impressive 44-year dividend streak and management has stated that they plan to increase the dividend by roughly 6% until 2022.

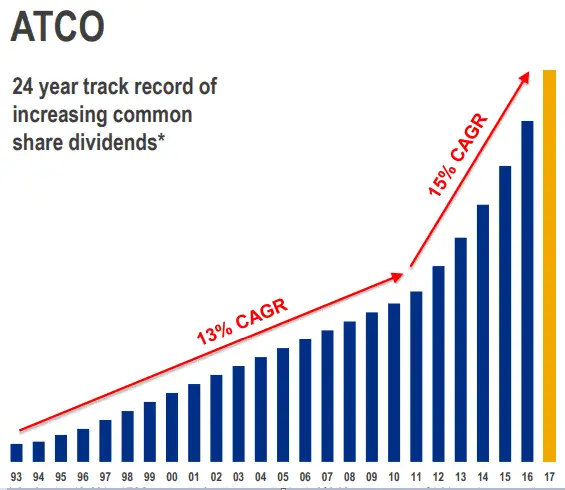

Atco Ltd.

Why it failed: Dividend yield was barely below 4% at 3.97% and future dividend growth estimate was under 6% at 4.6%.

With their relatively low payout ratio of 46.5% and their very strong dividend growth history, I think that the analyst estimates for dividend growth are low at 4.6%.

Source: February 2018 BMO Infrastructure & Utilities Conference Presentation

Atco’s most recent dividend increase was 15% and they have a 5 and 10-year dividend growth rate of 14.9% and 11.5%. Looking back over the past 15 years the lowest year over year dividend increase was 6%. I know past results don’t predict the future, but I expect better dividend growth than 4.6%.

If the price drops a bit more and Atco gets a 4% dividend yield I think the company is worthy of your consideration.

FYI – Atco owns 52% of Canadian Utilities Limited.

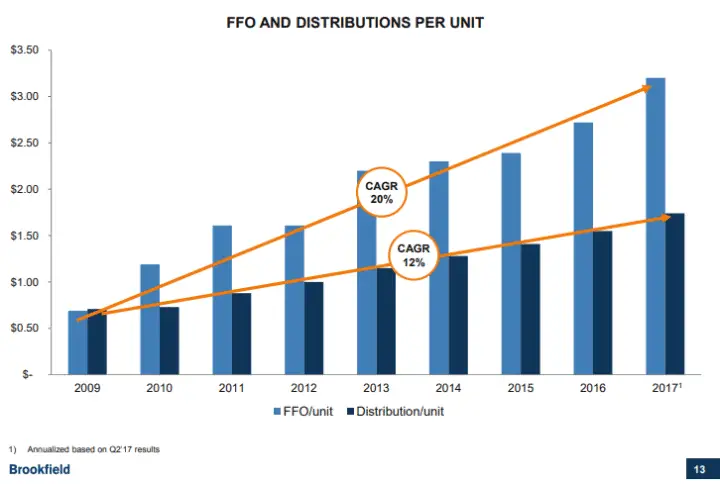

Brookfield Infrastructure Partners LP

Why it failed: EPS payout ratio was over 70% at 108.9%.

Brookfield Infrastructure isn’t a corporation and is structured as a limited partnership (LP) so it uses FFO instead of EPS to measure its success. As a result, it’s not really fair to use the EPS payout ratio, especially when Brookfield Infrastructure targets a payout ratio of 60-70% of FFO.

They have a 10-year dividend streak and a strong history of dividend growth.

Source: September 27, 2017 Investor Day Presentation

The LP is well run and is targeting 5-9% dividend growth and 12-15% returns. I’d expect dividend growth on the higher end of their 5-9% target.

Source: Investor Fact Sheet

With a BBB+ credit rating and strong targets from management, I think Brookfield Infrastructure Partners LP is worthy of your consideration. Just make sure you understand the added risks due to the limited partnership structure vs. a corporate structure.

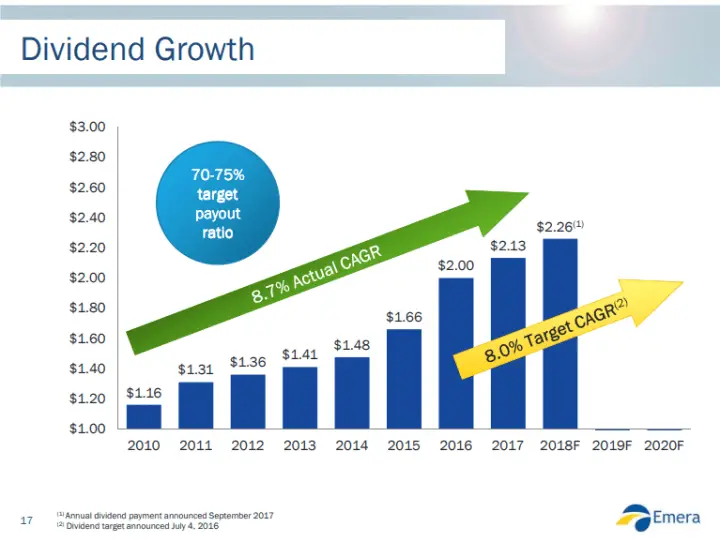

Emera

Why it failed: EPS payout ratio was too high at 82.4%, Moody’s rated them Baa3 and Thomson Reuters dividend growth estimate was under 6% at 4.4%.

The payout ratio is currently higher than my 70% target and also higher than Emera’s own target ratio of 70-75%.

Source: April 19, 2018 Investment Advisor Luncheon Presentation

A high payout ratio can be a sign that dividend growth is at risk, but in Emera’s case, they sound like they still plan for more 8% raises. Rob Hope; an analyst with Scotiabank, asked specifically about this in the May 11, 2018 earnings call:

Rob Hope: “moving over to the dividend in the MD&A, you reiterated the 8% growth commitment there. […] what about the dividend payout ratio? When would you expect to get back into your targeted range there?”

Greg Blunden, Emera CFO: “Nothing has changed from what we think is the long-term target where we’d like to be. Obviously, as a result primarily of U.S. tax reform, it’s unlikely that we’ll get there in 2018 and 2019. But we certainly see making meaningful progress, both this year and next year towards that path and targeting to get there by the end of the decade.”

It sounds like they still plan for 8% dividend growth to 2020 and this is also roughly when they plan to get back to their target payout ratio of 70-75%. If this is the case, then the Thomson Reuters dividend growth estimate of 4.4% might be a bit low and the Value Line dividend growth estimate of 8.5% might be a closer guess.

Moody’s rated them Baa3, but S&P rated them BBB+, so the average of the two is BBB which I think is reasonable for a utility, but I try not to go lower than this.

I think Emera is worthy of consideration, but it is a riskier choice from some of the other names as it has a lower credit profile and the payout ratio is on the high side. On the plus size, it has a high current dividend yield at 5.6%, an 11-year dividend streak, and potential for 8% dividend growth to 2020 if management comes through on its commitments.

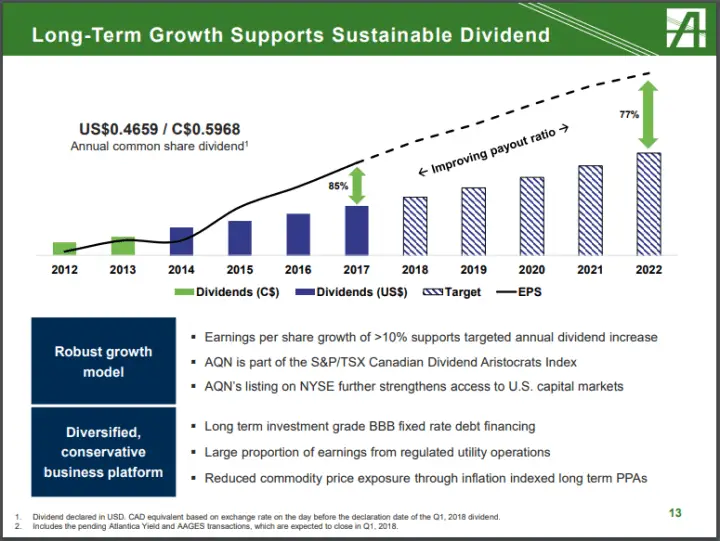

Algonquin Power & Utilities Corp.

Why it failed: EPS payout ratio was too high at 90.7% and DBRS rated them BBB (low).

Algonquin is a similar case to Emera; a high dividend yield at 5.3%, but a high payout ratio at 90.7%. Despite the high payout ratio, they still plan for high dividend growth. The plan is to increase the dividend annually at an impressive 10% until 2022 while growing earnings at a faster rate to slowly improve the payout ratio.

Source: March 2018 Investor Presentation

Where Algonquin differs from Emera is its slightly worse credit ratings and shorter dividend streak of 7 years. S&P rates Algonquin BBB and DBRS rates them BBB (low), so the average of the two is somewhere between BBB and BBB-. This is a little too low for me and I’d wait for a better credit rating before investing. If Algonquin is able to achieve their goals then it is likely fine, but a high payout ratio and a lower credit rating make it a riskier bet for long-term high dividend growth.

Should the credit rating improve then I think Algonquin is worth your consideration.

Losers:

Brookfield Renewable Energy Partners LP

Why it failed: High payout ratios based on EPS (355.1%) and FFO (88.6%). Dividend growth estimate was less than 6% at 5%.

Another Brookfield partnership, but unlike Brookfield Infrastructure Partners LP, the payout ratio appears too high and future dividend growth looks lower at 5%.

Brookfield Renewable Energy Partners LP is targeting an average FFO payout ratio of 70% and 5% to 9% annual growth in cash distributions. With an FFO payout ratio already above 70% at 88.6% I’d expect dividend growth at the low end of their 5-9% range. Analysts seem to agree and expect 5% dividend growth from 2018 to 2022. It’s also worth noting that their most recent dividend increase was on the low end of that range at 4.8%.

Brookfield Renewable Energy has a decent credit rating of BBB+ from S&P and BBB (high) from DBRS so I understand why there is interest in this high yielding stock with moderate dividend growth. Its current dividend yield of 6.3% is tempting with 5% dividend growth, but because of the added risks of the LP structure vs. a corporate structure and the high FFO payout ratio, I plan to pass for now.

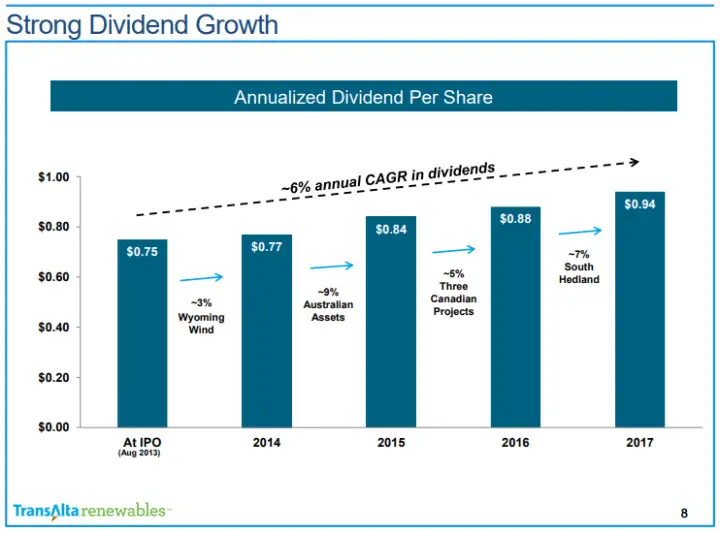

TransAlta Renewables Inc

Why it failed: No dividend growth expected in the future, and high payout ratios based on EPS and FFO.

TransAlta Renewables Inc. isn’t rated by any of the credit rating agencies, so I wasn’t able to get a quick read on its financial strength, but it failed three other metrics so I didn’t feel the need to spend much more time looking into it.

The high payout ratios; 116.5% EPS payout ratio and 76.5% FFO payout ratio, and no dividend growth estimated from analysts were enough to deter me. Despite the gloomy outlook, it’s actually had decent dividend growth since its IPO in 2013.

Source: March 2018 Investor Presentation

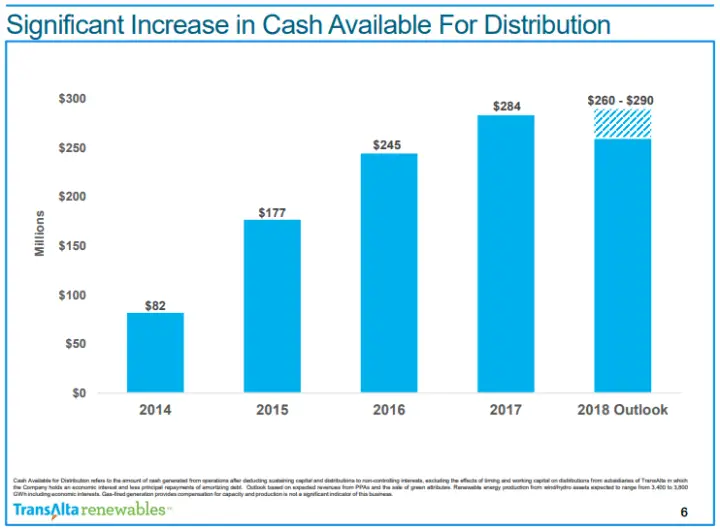

Its currently yielding a whopping 7.9%, so I think TransAlta Renewables will become a high yield low or no dividend growth company. I know analysts aren’t expecting any dividend growth, but I wouldn’t be surprised to see a small token raise.

Source: March 2018 Investor Presentation

In 2018 they are forecasting $260-$290 million in cash available for distribution. They have $250.1 million shares outstanding, so on a per share basis, they are forecasting $1.04 to $1.16 cash available for distribution.

Currently, they pay out $0.94 per share in dividends which is already 81.0% to 90.4% of their forecast without any future dividend growth. Say they met the high end of their outlook $290 million, that is still only 2% higher than 2017’s $284 million. All this tells me that in the short term they have a little room for smaller dividend increases, but in the long term, I don’t expect meaningful dividend growth.

The company also has a short dividend streak of 5 years as it’s IPO was in 2013. It hasn’t been tested during a recession. With such high payout ratios, they offer very little room to fund growth organically, instead, they are forced to either issue more shares or take on more debt. Companies can get away with this strategy for a while, but when times are tough these options aren’t always available or a reasonable alternative and that can lead to a dividend cut or no dividend growth.

The added risk of the high payout ratios and short history as a company are why I’ll be passing on this company and don’t think it is worth your consideration from a dividend growth perspective.

Summary

Utility companies typically have a high dividend yield and make good dividend growth candidates because they operate in a regulatory environment which limits competition and keeps earnings relatively predictable. These conditions result in utility companies typically having a narrow moat and are one of three sectors (Consumer Staples, Telecommunications, and Utilities) that have longer dividend streaks.

Utilities typically have a high yield but are more known for low to moderate dividend growth. It is important to try and identify the higher growth companies in this sector. That way we can meet the last of Lowell Miller’s dividend growth mantra: “High growth of dividends”.

Source: The Single Best Investment: Creating Wealth with Dividend Growth by Lowell Miller (Affiliate link, but I personally own and highly recommend this book.)

There are some appealing names in the Canadian market, but only one passed all of the dividend screen criteria: Canadian Utilities Limited. With its long history (46 years) of strong dividend growth that is expected to continue, its strong financial strength, and its high 5.1% dividend yield it is worthy of any dividend growth investor’s consideration.

Disclosure: I own shares of Canadian Utilities Ltd. and Emera Inc. You can see my portfolio here.

Newsletter Sign-Up & Bonus

Have you enjoyed our content?

Then subscribe to our newsletter and you'll be emailed more great content from Dividend Growth Investing & Retirement (DGI&R).

BONUS: Subscribe today and you'll be emailed the most recent version of the Canadian Dividend All-Star List (CDASL).

The CDASL is an excel spreadsheet with an abundance of useful dividend screening information on Canadian companies that have increased their dividend for five or more years in a row.

The CDASL is one of the most popular resources that DGI&R offers so don't miss out!

I tried to reply by email, but possibly this is the preferred way.

TD reports the payout ratio at 126%. This seems too high for comfort. You?

Most analysts rate the stock a HOLD. I’d prefer to see raving enthusiasm for the stock.

Finally, the current dividend yield plus CAGR of about 10% is certanly attractive.

Sorry, I received the email, I’m just a bit slow to respond these days with the baby.

The TD payout ratio for CU at 126% is probably the trailing twelve months ratio, whereas I used the next 12 months EPS estimate for my payout ratio. It’s a valid concern, but basically, I expect their EPS to improve.

Raving enthusiasm is nice because it helps validate your decision, but that won’t always result in the best returns. If everyone thinks something is great, then typically the price is higher. The other thing that is important to understand is that most analysts make their buy, sell or hold recommendations for a short-term outlook – in the next year or two. I invest for the long-term as I suspect you do too. Sometimes these conflict.

In the short-term, I suspect that they are worried about increasing interest rates and how that will affect utility stocks? It’s a fair concern as interest rates have been rising are expected to continue to rise (Keep in mind I like everyone else can’t predict the future). This could cause utility stocks to drop, or not who knows!

I invested in CU because it looked attractive at current levels. Will it drop more in the short-term? Maybe, but I’m a long-term investor, so I try to think in terms of decades.

Here’s a hypothetical for you. Say it doesn’t drop further I ended up not investing because I waited for a lower price that never came, how am I going to feel missing out on this? Or say I buy CU and it does drop further in the short term, in 10 or 20 years from now, will I be happy having purchased CU at +5% dividend yield with say 6-10% annual dividend growth (Just a guess)? I think I would be happy with that, but again I can’t predict the future. Obviously I’d like to be able to buy at the exact bottom, but I can’t predict when that is, so instead, I’m trying to find high-quality businesses with attractive dividend growth fundamentals and invest at reasonably cheap valuations. This company has the longest dividend streak in Canada, a credit rating around A, strong dividend growth, and high yield.

That’s my take on it, and why I decided to invest. But I’m a personal finance blogger… so it’s personal to me and not a recommendation to you. Everyone’s risk tolerances and circumstances are different so you have to do what’s best for YOU.

Cheers,

DGI&R

I am not a big fan of CU. I held it for while and it was going nowhere and dropped it. It has gone nowhere in recent years either.

I am guessing you are expecting something to change or you are just happy to get a dividend rate above the bond rate. In the current growing interest rate environment, investors in utilities are moving to bonds …

When do you expect to actually have a decent return?

Based on your total return formula from The Single Best Investment, (PDF is free on their website by the way), the Chowder Rule can be used to filter and BIP.UN comes on top for me followed by ACO.X, EMA and CU.

Cheers!

When do you expect to actually have a decent return?

I’m a long-term investor, so in a decade or two… My goals might be different from yours. I’m hoping to have dividend income cover some or all of my retirement expenses.

Cheers,

DGI&R

This was an excellent article, Much appreciated! I encourage you to issue more articles like this. Someone posted the article in the Facebook group called Canadian Dividend Investing, so that increased the readership. Please feel free to post future articles in this Facebook group.

Glad you liked the article and thanks for letting me know about the Facebook group.

Where did you find the Thomson Reuters dividend estimates?

Interactive Brokers is one of my online brokers which gives me access to Thomson Reuters analyst estimates.

I seem to have access to Thomson Reuters reports through Scotia Bank, but I can’t find any Dividend estimates. What do they call it?

I use interactive brokers (IB) for this info. Thomson Reuters compiles multiple analyst sources for the dividend average and median estimates and I get access through IB. I don’t think Scotia Bank provides the same info as it isn’t a report per se, but more of a data feed from Thomson Reuters.

Hi,

I noticed Altagas didn’t make the list. What are your thoughts on ALA.to as a dividend investment? Currently 8.5% yield.

It didn’t make this list as it is in the energy sector, even though they have some utilities. I haven’t looked at them in depth recently, but when I looked at them before I didn’t like that their EPS payout ratio was high and they had a credit rating that was a little to low for my liking. I’d like to see BBB+ or higher.

I understand the temptation though as they have a high yield and are planning to grow the dividend.