Dividend Growth Investing & Retirement is supported by its readers through donations and affiliate links. If you purchase through a link on my site, I may earn a commission. Thanks! Learn more.

One of the great benefits of this blog is that it keeps me honest and takes the moodiness out of my investing. Every time I buy or sell a stock I post a portfolio update. Having to justify my reasons for buying or selling a stock in these posts has made me a better investor. Thanks guys!

⭐ Find dividend growth stocks that have survived multiple recessions and increased dividends for 5, 10, 25+ years in a row.

I try and post these portfolio updates close to the time they happen, but I don’t always have time to write a full blog post, so they can be a bit delayed. For the most up to date portfolio updates follow me on twitter as I typically tweet the purchase/sale the same day it occurs and then write the blog post later.

Now on to the latest addition to my portfolio…

On June 29, 2015 I purchased shares of Exxon Mobil [XOM Trend] for $83.00 per share + commission. After commission my average price was $83.10. Exxon Mobil is an American multinational oil and gas corporation. I was excited to purchase shares for a number of reasons.

Dividend Champion

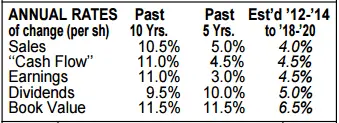

Exxon Mobil is dividend champion having raised their dividend for 33 years in a row. This is an impressive streak, made even better by their high dividend growth. Over the past 5 and 10 years they have increased the dividend at average annual rates of 10.0 and 9.5% respectively. Their most recent 5.8% dividend increase was announced at the end of April 2015. With all that is going on in the energy market right now it is encouraging to see Exxon Mobil continue to increase its dividend through these tough times. Not all companies have been able to do this. Chevron [CVX Trend]; another dividend champion, comes to mind as they were expected to announce a dividend increase in April 2015, but instead left it steady. In Chevron’s case I think they’ll get back to increasing the dividend in a few quarters, but if companies like Chevron are having trouble increasing their dividend it gives you an idea of the mayhem that oil prices are having in the market.

Wide Moat & Strong Financial Strength

Exxon Mobil is rated as a wide moat stock by Morningstar and is very financial strong. Value Line gives them an A++ financial strength rating and S&P rates them AAA. There are only two other US companies with a S&P AAA rating: Johnson & Johnson [JNJ Trend] and Microsoft [MSFT Trend].

With havoc in the oil market right now I want to invest in high quality companies that can survive and thrive. Knowing that I can sleep easy while the dividend continues to grow is an important part of my portfolio. As a long term investor a strong financial strength is very important to me. I want these companies to be around in a couple of decades so investing in an “iffy” company is not for me. Judging by Value Line and S&P ratings, I can rest easy.

Related article: Financial Strength: A Key Element in High Quality Dividend Growth Stocks

Future Dividend Growth

Currently Value Line is calling for average annual dividend growth of 5% for the next 3-5 years. I think over the longer term as oil prices improve dividend growth will be higher and more in line with their historic 5 and 10 year rates around 10%.

Valuation

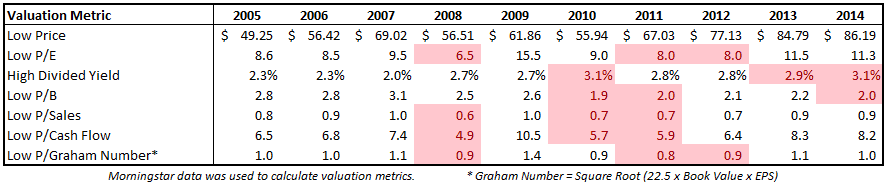

As with any purchase, valuation plays an important role. At $83 I feel like I got a reasonably cheap price for a quality stock like Exxon Mobil. Here’s a summary of valuation metrics for the past decade.

I like to focus on the lowest 3 valuations from the past decade (highlighted in red above). This is typically the range I like to target as reasonably cheap. For comparison’s sake I also include the median and average of the lowest valuation methods for the decade, and also the 5 year average valuations.

Looking at the above chart I might conclude that a reasonably cheap valuation for Exxon Mobil is a dividend yield of 2.9% to 3.1%. At $83 the dividend yield is 3.5% which is historically very high as it hasn’t reached these levels in the past decade. You can understand why I was excited to buy shares. 3.5% doesn’t sound like a very high dividend yield, but for Exxon Mobil it is.

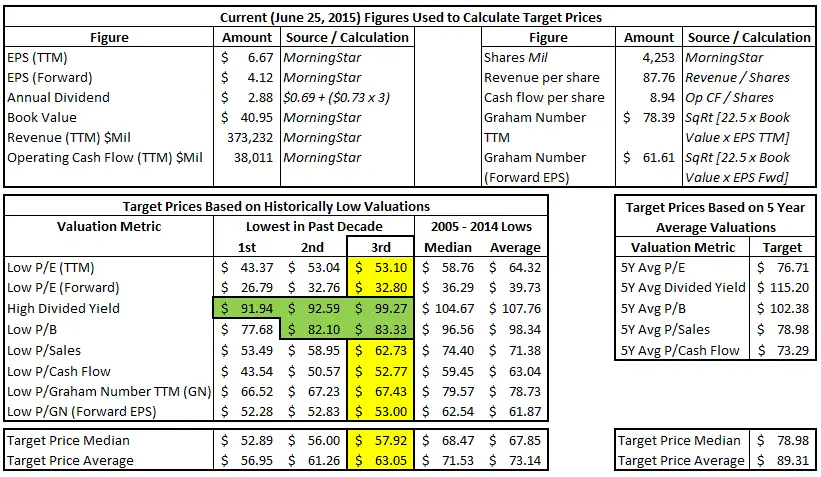

Now that a picture is starting form of what valuation ranges are historically cheap we can use these same figures to reverse calculate target prices using today’s figures.

At $83 my purchase is reasonably cheap when compared to the Price-per-book-value ratio (P/B) and dividend yield (green above), but not the others. Exxon Mobil’s sales, cash flow and earnings can fluctuate year to year because they are reliant to a certain extent on commodity (oil) prices. As a result these targets can vary widely from one year to the next, so I’m OK relying on the dividend yield and P/B ratio to determine a reasonably cheap price. To find a reasonably cheap price I will typically try and find a price that would fall in the third lowest valuation (yellow column) for two metrics. In this case it is dividend yield and P/B. As a dividend growth investor I usually rely more on dividend yield, but the more metrics that point to a cheap price the better.

From a valuation standpoint I think $83 is reasonably cheap for such a high quality dividend growth stock. I had a look at Morningstar’s valuation. Currently they rate Exxon Mobil as a 4 star stock with a 5 star price of $78.40. My purchase price isn’t far off the 5 star price, which is another good indication of a reasonable valuation.

What do you think of my Exxon Mobil purchase?

Photo credit: AK Rockefeller / Foter / CC BY-SA

Newsletter Sign-Up & Bonus

Have you enjoyed our content?

Then subscribe to our newsletter and you'll be emailed more great content from Dividend Growth Investing & Retirement (DGI&R).

BONUS: Subscribe today and you'll be emailed the most recent version of the Canadian Dividend All-Star List (CDASL).

The CDASL is an excel spreadsheet with an abundance of useful dividend screening information on Canadian companies that have increased their dividend for five or more years in a row.

The CDASL is one of the most popular resources that DGI&R offers so don't miss out!

Awesome! On Monday I’m going to buy a few shares.

Thanks

George

Hi George,

I’m glad you liked the post, but I have to be honest … comments like these scare me a bit. I post these portfolio updates so others can see why I am buying or selling a stock, but please don’t take these as stock recommendations. Always be sure to do your own due diligence before buying or selling a stock.

That said, assuming you have done the due diligence, I hope the investment works out us.

Cheers,

DGI&R

I’ve been thinking of buying XOM. Now seems to be a fairly good time. Thanks for the analysis.

Thanks for the breakdown of XOM. I really like it here and recently purchased some myself at around the 3.4% yield mark. I agree with you that CVX will return to dividend growth in the future, I don’t mind them being conservative here considering the consequences and pressures they are under. That being said I prefer XOM over CVX.

Excellent analysis of historical valuation data. On that basis, the stock is in an attractive buying range. In the past 10 yrs, XOM has trading below 70 many times and a few times below 60. A purchase at 83 is very likely a good long term bet. But don’t be scared out of the stock if it does drop into the 60’s.

The larger question is this: is the Oil / Gas industry entering a long new age of energy that is fundamentally different from the past 60 yrs? If there is a sea change afoot, how will XOM navigate those big shifts and continue to grow is EPS and Dividends/share?

I have owned XOM since 1981. No question it has been my best stock investment. XOM is surely the best managed integrated oil company, financially sound, superb project execution, solid technology. Management is inbred and well prepare to take over from retired execs. I see no evidence that XOM is losing its core management skills to cope with what ever the world throws at them. So for now I am holding on to my shares. For sure I would not sell XOM at these levels, … might even add a few shares if it drops into the 70’s if the market continues its decline into the Fall and Winter of 2015.

I really enjoy reading your updates and I appreciate their robustness and the effort you expend.

I’m inclined to agree with dcortez; I have my sights set on a lower entry level for XOM. I think BP represents better value at present at under $40.

Just curious do you guys not take into account buying US stocks now with the decline of our dollar? Perhaps you bought US dollars when the exchange rate was better?

I have been mostly ignoring it, but it is getting harder to as the Canadian dollar has been taking a beating. Rob Carrick wrote an interesting column over the weekend about hedging and noted that over the long term it doesn’t make that much of a difference: http://m.theglobeandmail.com/globe-investor/inside-the-market/should-i-protect-investments-in-us-markets-even-if-theyre-long-term/article25508347/?service=mobile.

I make a small amount of income in US dollars and i use my USD dividends to reinvest in more US stocks. This is sort of a natural hedge, but it is not enough of a hedge to cover the whole US stock purchase.

I’d say its in the back of mind when i make a purchase, but so far It hasn’t changed my target. That could change in the future though.