Dividend Growth Investing & Retirement is supported by its readers through donations and affiliate links. If you purchase through a link on my site, I may earn a commission. Thanks! Learn more.

Part of a successful life involves setting goals. It’s my plan to use this blog as a way of tracking and achieving my investing and early retirement goals. Setting goals for yourself can be a difficult thing, but I find it’s best to start with the big picture idea.

Big Picture Goal:

⭐ Find dividend growth stocks that have survived multiple recessions and increased dividends for 5, 10, 25+ years in a row.

When setting goals it is important that they are achievable, but also ambitious. You want a goal to strive for, but at the same time you don’t want it to be way out there otherwise you will get demoralized because it’s too unrealistic. For me, big picture, the goal is early retirement. OK, so that’s out of the way, what next? Big picture goals are a great start, but they are usually too vague just by themselves. When goal setting, it is important to have a measurable goal. If you can’t track your progress and adjust accordingly it is less likely you will reach your goal. This is especially true for long term goals. Having a measurable goal with a plan will improve the likelihood of succeeding.

Measurable Goal:

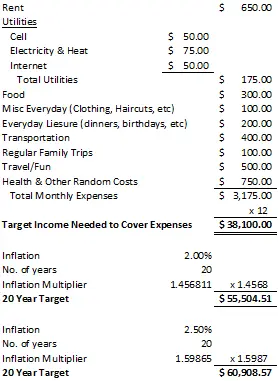

I want to be able to retire in 20 years. Having a timeline of 20 years is fine, but we can still do better. You have to think about the goal and what it means to you. For me, retirement means financial independence. I want my expenses to be covered by passive income so my time is truly mine. This does not necessarily mean that I won’t be working after 46, but the point is that it’ll be up to me and I won’t have to worry about it from a financial perspective. Now that we have a clear idea of what retirement means to me the next thing is to quantify it. This can be quite difficult as we are trying to find a target 20 years out. It is unlikely you are going to accurately predict 20 years into the future, but just do as best as you can. I did a quick budget and added in inflation of 2% to 2.5% and came up with $60,000. This is the amount of annual passive income I’d need to retire in 20 years. So now the goal to retire early can be measured by my two criteria: retire in 20 years, and have $60,000 of passive income. Now that my goal is sufficiently measurable I can move on to the next step: Planning. (You can take a look at the budget and inflation calculations at the end of this post.)

Planning:

We now know that I want to achieve financial freedom, by having a annual passive income of $60,000 before my 47th birthday. That all sounds great, but how am I going to do this? I hope to meet my goals by investing in dividend growth stocks and using the income to live off on in retirement. Currently I have about $50,000 invested. I have about $10,000 in cash that I plan to invest this year. I’m currently on a one year leave from my regular work on a working holiday with my girlfriend. With my travel expenses I’m not expecting to be able to contribute more than $10,000 for 2013. I go back to my regular job in October, at which point I’ll be able to contribute more. Over the past two years prior to travelling, I’d been able to save $20,000 per year by aggressively saving and reducing expenses, so I think it’s realistic I can continue this trend when I’m back in Canada. After five years I hope to be able to increase my annual savings to $25,000 per year.

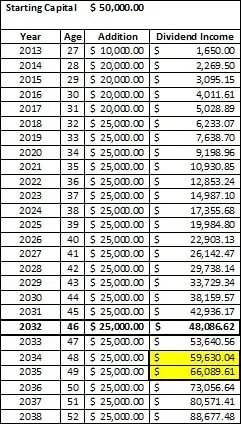

I ran the number and came up the following. I used an average dividend yield of 3%, and a dividend growth rate of 8%. All the dividends that I receive prior to retirement I am assuming will be reinvested.

From these calculations it looks like I’d have $48,000 when I’m 46, which is $12,000 short of my goal. Just two years later I would get very close to $60,000 though (yellow highlighted amounts). So to reach my goal, I’ll have to contribute a bit extra over the 20 years. As I mentioned before; when setting goals it is important that they are achievable, but also ambitious. I feel like this plan fits that bill quite well. By pushing myself I should be able to reach financial freedom by 46. Now to put the plan into action.

Action, Review and Adjustments:

When setting long term goals you have to be flexible, as a lot can happen in 20 years. It’s important to track your progress and see how aligned you are with your plan. Review your goals on a regular basis and make adjustments if necessary. I imagine things will pop over the next 20 years, that will force me to adjust and adapt. One thing that comes to mind, is children. I’d like to have two kids. Maintaining my high level of savings could be problematic once the little guys show up. Whenever this happens, I’ll have to adjust the plan accordingly.

Final Thoughts:

Goals can be a powerful tool when used properly. Probably where most people fail when it comes to goals is not spending enough time in the planning and action stages. Think of all those New Year’s resolutions that fall apart sometime in February. It’s easy enough to state a goal, but to stick with it is harder. It also helps if you can describe what you are doing in one sentence. For instance

I buy reasonably to cheaply priced companies that have a history of paying and sustaining increasing dividends in order to support my early retirement goals.

A clear statement like this, lets others easily understand what you are trying to achieve.

So what do you think of my early retirement goal? Can it be done, or am I delusional?

Appendix: My Retirement Expense Budget:

I made up a budget of the expenses that I’ll need covered in retirement. Over the next 20 years I expect this will change quite drastically, but I feel it’s a fair budget based on my spending habits.

I should also mention some of my assumptions in this budget as it is by no means perfect. This budget is my estimated costs in a relationship. That means that there is someone else in the picture paying the other half. The rent I set at $650 and I feel it’s reasonable, but I might not always be renting. Who knows I’ll be doing that for the next 20 years. I’m not as enamored with home ownership as most Canadians, because I like flexibility and I feel that better returns can be made in the stock market as opposed to a house/property you buy. Once I have kids this may change. Generally I wouldn’t recommend buying a place unless you know you’ll be there for more than at least five years, 10 years would be better. I can’t currently say this, so I’ll stick with renting. The other major reason I’m not that interested in buying a house is that I’d be buying in Vancouver, which in my opinion is in a bubble along with the rest of the Canadian real estate market. I’d like to see prices come down before I buy a place. I have absolutely no experience in real estate, so take this with a grain of salt. Anyways, back to the rent… Over the next 20 years at some point I imagine I’ll buy some property, but I want the mortgage to be paid off by the time I retire. If the mortgage is paid off at the time of retirement then I wouldn’t be paying rent, but I’d have to pay maintenance, property taxes, etc. I ended up deciding that I’d leave it at $650 as it should cover me either way.

I’d like to be able to do some travelling in retirement, so I set this at $500 per month.

I set $750 for Health and other random expenses that pop up. This is my catch all category, as you can’t predict all expenses. I think $750 a month is more than fair.

For inflation I ran the numbers using 2.0% and 2.5%. I ended up deciding $60,000 was a reasonable target as this is in the upper range of the 2.0-2.5% inflation. I have no idea what inflation will be in the future, but 2.5% in the past has seemed reasonable.

One thing this budget doesn’t take into account is taxes. Also because I plan to retire well before 65 or 67 I didn’t bother factoring in CPP, OAS, or company pensions. Normally you would factor these in, but I don’t mind the added conservatism.

Newsletter Sign-Up & Bonus

Have you enjoyed our content?

Then subscribe to our newsletter and you'll be emailed more great content from Dividend Growth Investing & Retirement (DGI&R).

BONUS: Subscribe today and you'll be emailed the most recent version of the Canadian Dividend All-Star List (CDASL).

The CDASL is an excel spreadsheet with an abundance of useful dividend screening information on Canadian companies that have increased their dividend for five or more years in a row.

The CDASL is one of the most popular resources that DGI&R offers so don't miss out!

Hi DGIR;

I am approaching retirement soon myself.

I don’t think your budget is quite high enough but I don’t know your life plans (children?) nor life style.

I have budgeted for approx 38.5K net per year as a means to sustain what I hope will be a relaxing but not extravagant lifestyle. I own a home so taxes and utilities are a major factor. I hope to take one nice vacation per year. I have over budgeted for some items like utilities as I would rather tote up projected costs rather than run by the skin of my teeth right off the bat. That way I won’t have to turn down the house heat right away. LOL

I figure approx $55.5 gross to to give me the $38.5 net. All of this is just conjecture until I am off the pay roll.

One other thing to consider is that if you set up RIF’s you will have minimum withdrawal rates to adher to. At 48 they will be neglible but will have to be met. You can check the gov can website for the rates. This is a major factor for me as I am older so the minimum rate is higher and may be more than I really want or need (7.38% at 71 yrs). This obviously depends on the value of your RRSP’s. So you may want to have several RRSP’s so that you do not have to convert 100% in to a RIF. That way you can stagger the RIF until you are 71 and you HAVE to have them all in RIF’s

O fcourse having non registered funds avaiable at yur projected retirement age would be a God send as you would not have to touch your RRSP’s.

I am hoping to run three to four years on non registered funds along with CPP and OAS and a very small company pension before I have to draw down the RRSP’s. During that time they can continue to grow with re-invested dividends.

Appreciate your articles

You are probably right that my budget is a little low, but I just did the best with the information I had at the time. Since then, my life has changed. I’m getting married soon and kids are somewhere down the line, so this budget will need to be adjusted for the changes in my life. When it comes down to it, you can only predict so much. Looking 20-30 years down the road is near impossible, so I try and focus on things I can control right now, like saving a large portion of income and investing it.