Dividend Growth Investing & Retirement is supported by its readers through donations and affiliate links. If you purchase through a link on my site, I may earn a commission. Thanks! Learn more.

So first let me apologize … this article is over 4,000 words. I could have split this analysis into multiple articles, but when I read other blogs I like it when all the information is in one place so I kept this as one big article. Feel free to jump around to the areas you are interested in as there are four general topics:

⭐ Find dividend growth stocks that have survived multiple recessions and increased dividends for 5, 10, 25+ years in a row.

- Overall dividend stock analysis of Home Capital Group Inc.

- Financial strength & stress testing of the company.

- Why I’d consider investing in the company when I think the housing market is over-valued.

- Home Capital Group Inc. valuation metrics.

Company Description

Home Capital Group Inc. [TSE:HCG Trend] is a Canadian holding company that operates primarily through its federally regulated subsidiary Home Trust Company, a non-traditional mortgage lender. They are Canada’s largest alternative mortgage lender. Home Capital Group Inc.’s main source of income is from residential mortgage lending, but they also offer non-residential mortgage lending, consumer lending and credit card products. Their mortgages are a mix of uninsured mortgages and securitized mortgages that are insured by Canada Mortgage Housing Corp. or other mortgage insurers. The uninsured mortgages are made with people that the big banks won’t give a mortgage to. These can include recent immigrants without a long enough credit history and some business owners. Home Trust offers services across Canada, but they do the majority of their business in Ontario.

In addition, Home Trust offers deposits via brokers and financial planners, and through its direct to consumer deposit brand, Oaken Financial. The Company’s subsidiary, Payment Services Interactive Gateway Inc. (PSiGate), provides payment card services. Their website is http://www.homecapital.com/

10 Year Stock Chart

Looking at the 10 year stock chart, there is a 10 year annual average return of 8.8%. If we include the dividend payments over the past 10 fiscal years (Total dividends paid of $3.37) then the total average annual return would be 9.7% with the average return from dividends representing 0.9%.

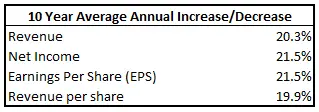

Revenue and Earnings

Home Capital Group Inc. has impressive earnings and revenue growth. I get the following growth rates based on the most recent year end (December 31, 2014).

All rates are around 20% which is well above the 8% I typically look for. Having high growth rates are good, but I also like to see that they have a history of increasing earnings year after year on a consistent basis. I like to see revenue and net income steadily increasing over time. I will allow the odd blip, but I don’t like to see erratic earnings. I like companies that make more and more money over time, and do not have losses.

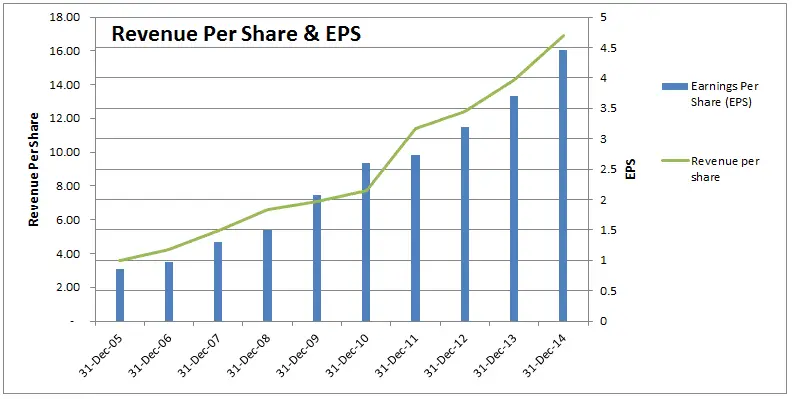

You can see from the chart above that revenue and net income have increased at a very consistent basis. Both revenue and net income have increased each year over the prior for the past decade. The same can be said for revenue per share and EPS as seen the chart below.

Related article: 14 Canadian Dividend Growth Companies with Consistently High Earnings Growth

So we have high consistent earnings and revenue growth all well above 8%. So far Home Capital Group Inc. is looking good. Next we’ll look at the dividends.

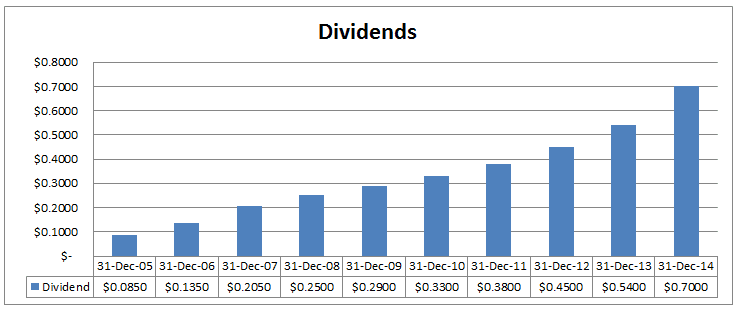

Dividends

A quick look at the Canadian Dividend All-Star List tells me that Home Capital Group has increased their dividend for 16 consecutive calendar years in a row which is a good dividend streak.

Related: Canadian Dividend All-Star List

Their most recent dividend increase was the dividend recorded in February 2015 when they increased the quarterly dividend by 10.0% from $0.20 to $0.22. The company has been increasing their dividend more than once a year, so the February increase was actually an annual increase of 37.5% as a year before the quarterly dividend was $0.16.

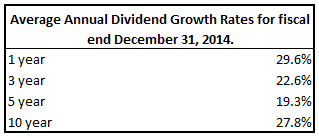

Dividend Growth

As you can see from the table below Home Capital Group Inc. shows some very strong average annual dividend growth rates.

With the most recent dividend increases it looks like they plan on continuing high levels of dividend growth. Now let’s see if the dividend is sustainable.

Dividend Sustainability

The 10 year average annual dividend growth has been higher than EPS growth which suggests that eventually dividend growth should slow down.

Let’s take a look at the payout ratio to see how much room for growth the dividend still has.

The company has been increasing dividends faster than earnings, but because they have a low payout ratio the dividend appears sustainable for the time being. The payout ratio has increased over the past decade from about 10% to around 16%, but it is still quite low overall. I consider a payout ratio under 30% to be quite low.

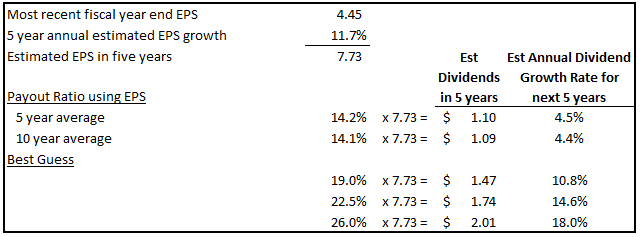

Estimated 5 Year Future Dividend Growth

It’s important to look to the future as well as to the past. I’m generally looking for companies with an 8% dividend growth rate. In order for a company to sustain this level of dividend growth I want to see that their estimated earnings are above 8%. It’s best to take these estimates with a grain of salt as a lot can happen in 5 years, and the further away the estimate the less accurate it gets.

Analysts expect annual EPS growth to be 11.69% for the next 5 years and the company stated in the 2014 annual report that their mid-term (3 to 5 years) objectives are to:

- “Achieve, on average, annual growth in diluted earnings per share (adjusted) of 8% to 13%;

- Achieve, on average, annual return on equity in excess of 20%;

- Maintain strong capital ratios that exceed regulatory minimums by a safe margin commensurate with our risk profile; and

- Pay out, on average, 19% to 26% of our profits as dividends to shareholders.”

Having these mid-term objectives makes it a little easier to estimate future dividend growth. It also helps that the analysts are estimating EPS growth of 11.69% which is in line with the company’s objective of 8% to 13% EPS growth over the next 3 to 5 years.

Based on the current $0.88 annual dividend it looks like annual dividend growth of roughly 11% to 18% is conceivable if the company meets its earnings growth targets. This is well above the 8% I typically look for. So far Home Capital Group Inc. is looking like a strong dividend growth stock.

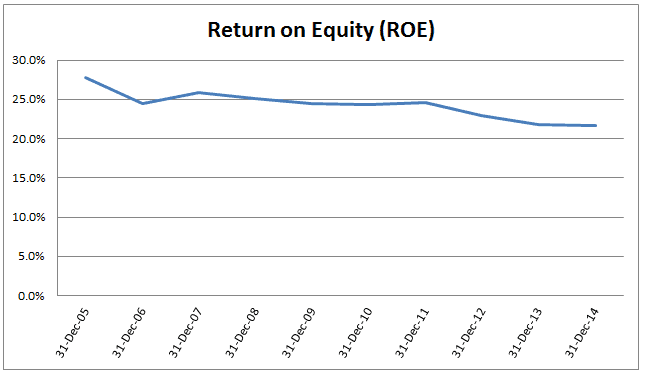

Competitive Advantage & Return on Equity (ROE)

The company has a history of high ROE. As you can see they have had a ROE over 20% for the past decade. In fact according to their 2014 annual report 2014 was their 17th consecutive year with ROE of over 20%. ROE has been slowly decreasing over the past decade, but they have consistently been over 20% which is very good. Finding companies with over 20% ROE for a decade, let alone 17 years is quite difficult.

I’d expect this trend of above 20% ROE to continue as it is one of their mid-term objectives and they have a compelling history of meeting this objective.

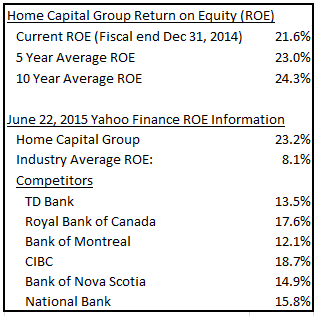

ROE is a good signal of a competitive advantage, but that in of itself doesn’t necessary mean one exists. In Home Capital Group’s case I’m not sure if the company has a competitive advantage or if it is just a well-run company. Its competitors are other mortgage lenders in Canada which include smaller companies and the big banks. I thought it would be interesting to compare it to the big banks which are considered to have a competitive advantage in the Canadian market even though the business in not entirely the same.

Currently Home Capital Group has a higher ROE than all of the big Canadian banks and its ROE is well above the Mortgage Investment industry average of 8.1%. The 8.1% is from Yahoo Finance, but I think it mostly used data from US companies. As Home Capital operates in Canada, I’m not sure if the 8.1% is a great comparison. These numbers suggest some sort of advantage, but at this point I don’t have a definitive answer on whether the company has a sustainable competitive advantage or not. I think they probably do. Based on the numbers I’ve reviewed so far I’d be OK investing in the company at a reasonable price.

Financial Strength

Assessing the financial strength of a bank or mortgage lender is quite difficult. Ratios like debt to equity are often much higher than other industries because of the nature of the business. This makes it harder to assess financial strength in the normal fashion. For Home Capital Group I’ve assessed financial strength by breaking it down into four categories:

- Debt Ratings,

- Basel III Requirements,

- Loan to Value (LTV) Ratios, and

- Stress Testing & Risks.

Let’s see what the rating agencies have to say about Home Capital Group Inc.’s debt.

Debt Ratings

I was able to find debt ratings from Standard & Poor’s (S&P) and DBRS in the company’s annual information form. As of December 31, 2014 S&P and DBRS had the following ratings:

Home Capital Group Inc. has investment grade long term ratings along with its subsidiary Home Trust Company which is rated slightly better. So what does this mean? I was able to find the following also in the annual information form which addressed S&P’s long-term rating:

“An obligor rated ‘BBB’ has adequate capacity to meet its financial commitments. However, adverse economic conditions or changing circumstances are more likely to lead to a weakened capacity of the obligor to meet its financial commitments. The “+” or “-” symbols show relative standing within the rating category.”

Basically they are doing fine, but they could be doing better. If the economy were to collapse or say the Ontario real estate market crashed then this company would struggle. Based on how well they handled the financial crisis of 2008 and 2009 and the stress testing they complete, I think the company would survive and ultimately get back to their old self, but it would be a painful period for them.

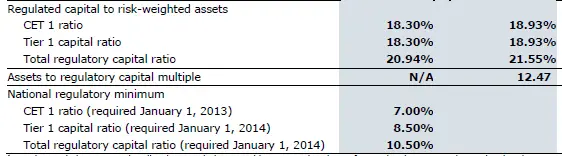

Basel III Requirements

Basel III requirements were developed by the Basel Committee on Banking Supervision in response to the 2008 to 2009 financial crisis. These requirements are meant to improve the banking sector’s ability to deal with financial and economic stress, improve risk management and strengthen the banks’ transparency. You can see from the table 32 in the 2014 annual report that Home Trust Company (Home Capital Group’s subsidiary) is well above the Basel III requirements. This is a good sign.

Basel III Regulatory Capital (Based only on the subsidiary, Home Trust Company)

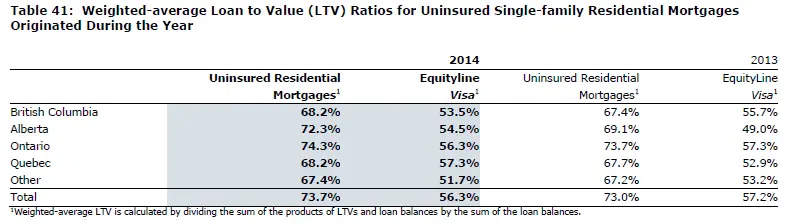

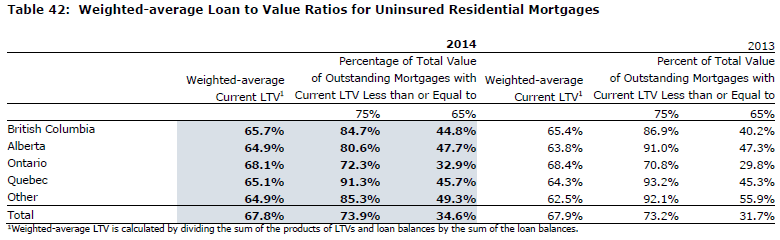

Loan to Value (LTV) Ratio

A customer is less likely to default if their equity in the property is high. This is why a lower loan to value ratio (LTV) is better. The LTV ratio is the mortgage value dividend by the value of the property. Home Capital Group tries to target low LTV ratios to reduce the risk of default. I’ve included two tables below from the 2014 annual report that shed some light on Home Capital Group’s mortgage portfolio.

From the two tables above you can see that in 2014 that the average LTV ratio of uninsured residential mortgages originated during the year was 73.7%, and the average for all uninsured residential mortgages was 67.8%.

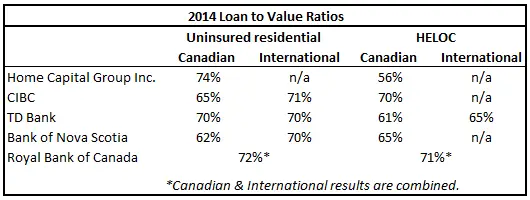

I had a look at some of the Canadian banks to get an idea of what LTV ratios they had for loans originated in the year.

Home Capital Group is in the same ballpark, but still has the highest LTV. This makes sense as Home Capital Group takes a bit more risk than the banks typically do.

Stress Testing & Risks

The company does regular stress testing and from the 2014 annual report I was able to find out what types of scenarios they stress test.

“Management has evaluated a range of stress scenarios, including a real estate driven recession, a natural disaster, a recession in oil producing regions, a condominium and commercial downturn, and a reverse stress scenario. Management analyzes the outcomes from stress testing and, where applicable, takes proactive measures to mitigate potential risks to the business.”

I tried contacting their investor relations department for their stress testing results, but they keep these reports internal. I did find one article written by Michael McCloskey in August 2012 that was posted in the Globe & Mail and Seeking Alpha that shed some light on the topic. The article mentioned that from one of Home Capital Group’s stress tests they assumed unemployment was at 10% and the real estate market crashed by 45%.

I’m not an economist so I wanted to get a better idea of what 10% unemployment looked like historically. During the last financial crisis we can see the jump in unemployment in 2009 to just under 9%. I thought based on this a 10% unemployment rate was a reasonable scary situation to run a stress test with. The chart and quote below came from http://www.tradingeconomics.com/canada/unemployment-rate

“Unemployment Rate in Canada averaged 7.73 percent from 1966 until 2015, reaching an all time high of 13.10 percent in December of 1982 and a record low of 2.90 percent in June of 1966. Unemployment Rate in Canada is reported by the Statistics Canada.”

Now that we have a better understanding of historical unemployment rates let’s get back to Home Capital Group’s stress test where they assumed unemployment was 10% and the real estate market crashed by 45%. In this scenario they estimated that they would survive, but loose one year’s worth of earnings. Michael McCloskey completed his own stress test and assumed that real estate prices fell by 50%. In Mr. McCloskey’s stress test he figured that by “Using default rate and loss assumptions that are significantly higher than Home Capital’s historical experience,” […] “the company would lose two to three quarters’ worth of earnings.”

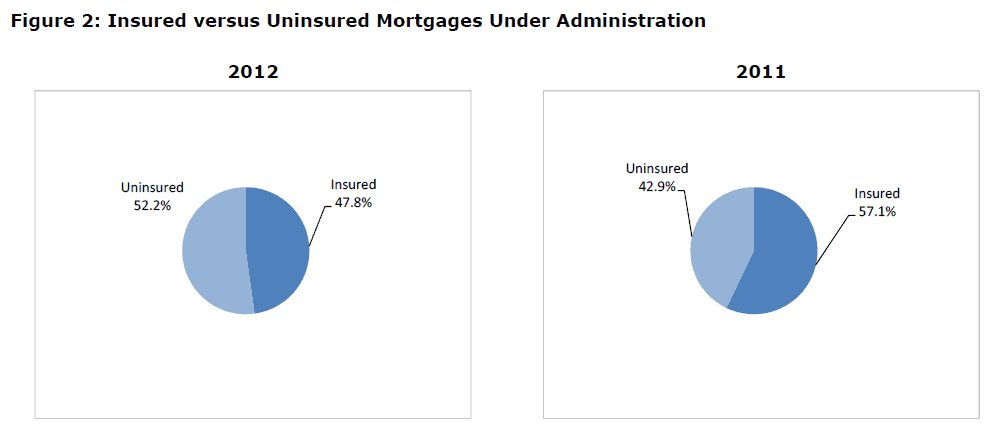

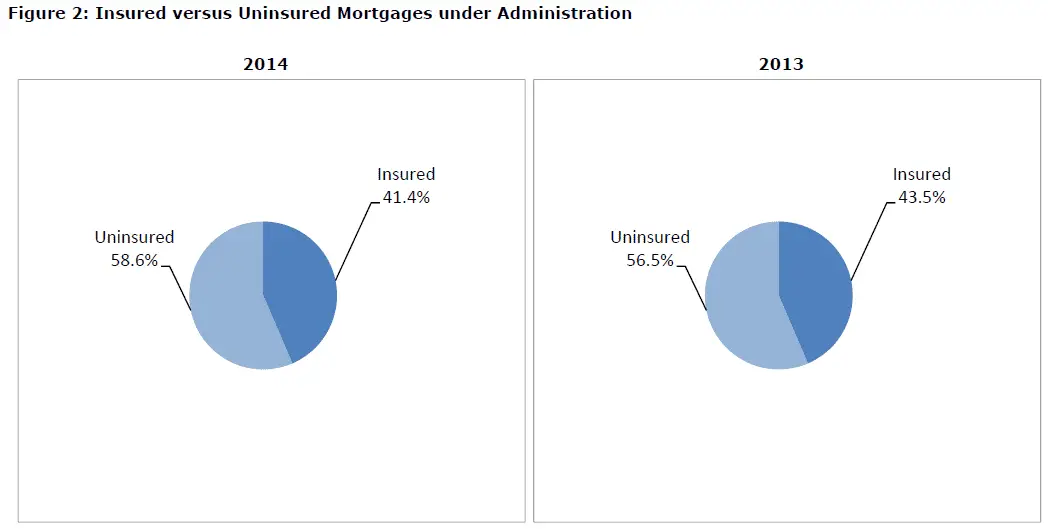

Based on the date of the article I’m assuming these stress tests were completed using either 2011 or 2012 data. This is important because Home Capital’s uninsured loan portfolio has increased since then. You can see in the charts from the 2012 annual report that in 2011 the uninsured portion was 42.9% and in 2012 it was 52.2%.

For the year end 2014 it was 58.6%, which is 37% higher than 2011 and 12% higher than 2012.

I did a crude extrapolation using the more conservative 37% increase from 2011 to 2014 from the previous stress tests. Because of a larger portfolio of uninsured loans the company could expect to lose about one year and 4 or 5 months’ worth of earnings. This was extrapolated from Home Capital’s 10% unemployment and 45% real estate market crash scenario that originally said they’d lose about a year’s worth of earnings. Mr. McCloskey’s scenario of 50% real estate market crash would extrapolate to 3 to 4 quarters worth of lost earnings from the original 2 to 3 quarters. These extrapolations don’t take into consideration the loan to value ratios that have been increasing.

Since the stress tests that were completed in August 2012 the LTV ratios on residential mortgages have been creeping up as you can see in the table below.

With this increase in LTV rates originated in the year, I’d expect today’s mortgages to be more risky than when the stress tests were first completed. Based on this and my extrapolation from before my final estimate would be a loss equivalent to a year or two of lost earnings, likely closer to a year to a year and a half if the housing market were to collapse.

With a larger portion of uninsured loans and the company accepting higher LTV mortgages they are more susceptible to risk and losses versus the insured loans. These stress tests show that while it wouldn’t be a fun time for the company they would likely survive. A big caveat is that I’m extrapolating from 2011 or 2012 data. I mentioned that it was a crude extrapolation because the company and the economy have changed since then and I have largely ignored these changes.

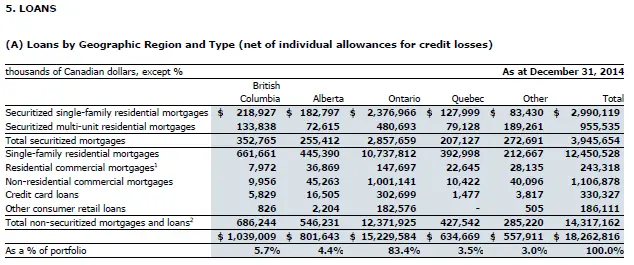

Whether or not a real estate crash is coming can’t be known, but it’s a valid risk. Because Home Capital has a large portion of loans in Ontario they are most susceptible to fluctuations in the Ontario market. You can see from the loans table from the 2014 annual report that over 80% of their loans are in Ontario.

If the Ontario real estate market crashed it would hurt the company the most as this is where it does most of its business. If you think Toronto and the Ontario real estate market are due for a correction or crash, then now is probably not the time to go out and buy shares. I don’t pretend to be an expert on the real estate market, so you’ll have to make your own decision on this.

You’ll notice that Alberta is 4.4% of the loan portfolio and some 32% of these are insured, so I don’t expect the recent oil price drops and the havoc they are reaping to overly affect the company.

Financial Strength Summary

If you made it through the last 1,400 words or so, you’ll notice that it was all about the company’s financial strength. Normally I don’t devote this much attention to this section, but for Home Capital Group Inc. I felt it was warranted. The biggest risk right now that I see for this company is a real estate market crash in Canada as the market appears over-valued. Naturally I wanted to see if the company could withstand a market crash. I think they can, but based on my stress testing they’d lose the equivalent of a year or two in lost earnings.

Another important question that I wanted answered was: “If there was a market crash would they have to cut the dividend?” If there was a crash I don’t think they would cut the dividend, but wouldn’t be surprised if they kept it steady for a bit as they weathered the storm. They have a low payout ratio which gives them more room to maneuver when times get tough. For me this is important because I don’t want to invest in a company, have the market crash, the stock plummet, and then have the dividend get cut. When a company cuts their dividend I sell the stock, so this would force me to sell the company at a low price. I want a company that can weather the storm and then get back to increasing the dividend.

I think Home Capital Group overall has good financial strength, but not great. At this point it is enough for me to consider investing in the company, but it could be better.

Why Consider Investing if the Housing Market is Over-Valued?

At this point you may be wondering why I’d consider investing in this company if I think the housing market is over-valued. It comes down to timing and valuation for me. Trying to predict when a macro event like a housing crash will occur is hard enough for the professional economists, let alone me. Rather than trying to predict the future I prefer to focus on individual companies. If a stock looks reasonably cheap and it is a strong dividend growth company then odds are I’ll consider buying it. If it turns out that the crash comes the next day, then I’d likely just buy some more of it as it has become even cheaper.

I read a great article by Nelson Smith of Financial Uproar called F- You I’m Short Your House. The article; written in 2013, lays out a very convincing case on why the author thinks the Canadian housing market is over-valued and why he decided to short the Canadian banks. He even considers shorting Home Capital Group in the article. Flash forward two years and those same convincing stats have only gotten worse as the crash never came and the market continued to go up for the most part. His fundamental analysis may be convincing, but the market didn’t react as expected and Nelson ended up losing money on his short because the timing was off. Trying to guess when a bubble will burst is very hard as the market can be over or under valued for long periods of time. This is why “timing the market” is generally not a great idea.

With macro trends like a house over-valuation it can be very difficult to predict when or if it will correct, crash, or just do nothing. As a long term investor I’m not trying to predict when the next crash will occur and profit through a one-time macro event. I prefer to focus on individual companies and whether they’d be able to survive and provide a long term benefit to my portfolio. My ideal holding period is forever as I’m trying to grow the dividend income of my portfolio to fund retirement. With such a long holding period it is inevitable that at some point there will be a crash of some sort that the company will have to go through. Rather than focus on trying to predict the future I try and analyze if the company can survive these crashes and over the long term make materially more money so they can continue to grow the dividend. If they are a strong dividend growth candidate and they pass these tests, then I try and purchase them at reasonably cheap valuations. This is why I recently purchased Home Capital Group Inc. for $41 even though the housing market appears over-valued.

Related article: Bird Poop & Portfolio Update: Home Capital Group Inc. Purchased

Valuation

There are a lot of different ways to value of company some of them better than others. Rather than focus solely on one method I like to use a variety of methods and compare the results to find a reasonably cheap price range to buy at. As a dividend growth investor I usually rely more heavily on dividend yield as a valuation method.

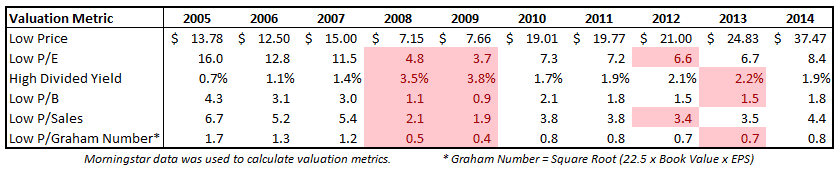

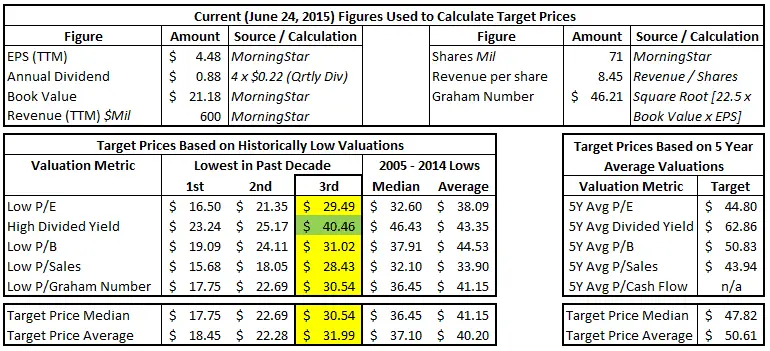

To start with I like to look at the past decade and calculate the lowest price and valuations for each year to get an idea of what was considered cheap in the past.

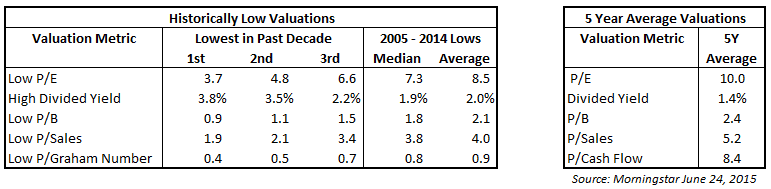

From here I like to focus on the lowest 3 valuations from the past decade (highlighted in red above). This is typically the range I like to target as reasonably cheap. For comparison’s sake I also include the median and average of the lowest valuation methods for the decade, and also the 5 year average valuations.

Looking at the above chart I might conclude that a reasonably cheap valuation for Home Capital Group Inc. is a dividend yield of 2.2% to 3.8%. This range is at least 20% above the 2005 – 2014 low average (2.0%) and median (1.9%), and well above the 5 year average dividend yield of 1.4%. These comparisons help me analyze if my range is reasonably cheap.

Now that a picture is starting form of what valuation ranges are historically cheap we can use these same figures to reverse calculate target prices using today’s figures.

I usually focus on the target prices from the third lowest valuation metrics (highlighted in yellow and green above). I mentioned before that I tend to focus on dividend yield as I’m a dividend growth investor and you’ll see that the target is $40.46 (highlighted above in green). I used this target rounded up to $41 when I made the decision to buy shares in Home Capital Group Inc. on June 16, 2015.

Related article: Bird Poop & Portfolio Update: Home Capital Group Inc. Purchased

You’ll notice that the targets based on the dividend yield are the highest among the various valuation methods, so you might consider using a different valuation metric or combination of them to come up with your own target. For instance I think that $41 is a reasonably cheap target, but if you wanted to be more conservative you might go with $31-$32 which is closer to the median and average for the 3rd lowest in the past decade.

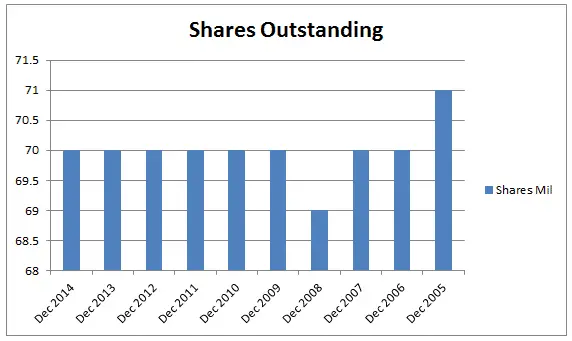

Shares Outstanding

Shares outstanding have basically been the same for the past decade. It’s nice when shares decrease over time, but I’m more interested in dividend growth which the company has been great with.

Conclusion

I think Home Capital Group Inc. strong dividend growth company. They have a dividend profile of low yield and high dividend growth. Normally I like to have a starting dividend yield of at least a 2.5%, but because of their high dividend growth I’m willing to invest in them at a dividend yield of 2.2%. They have increased their dividend for the past 16 consecutive calendar years and have high 5 and 10 year dividend growth rates of 19% and 28%. Their payout ratio; at about 20%, is low which should allow the dividend to continue to grow at high rates. The company has mid-term goals to grow earnings annually by 8% to 13%. This coupled with their target payout ratio to 19% to 26% suggests high future dividend growth of 11% to 18% per year. The company has good financial strength and has managed 17 consecutive years of a ROE of over 20%.

The main risk I see for the company is an over-valued housing market and the potential for a housing crash. Based on my stress testing they could survive a market crash, but it would not be a fun as they’d likely lose the equivalent of a year or two in earnings. Rather than trying to predict the future I try and analyze if the company can survive these crashes and over the long term make materially more money so they can continue to grow the dividend. If they are a strong dividend growth candidate and they pass these tests, then I try and purchase them at reasonably cheap valuations. This is why I recently purchased Home Capital Group Inc. for $41 even though the housing market appears over-valued.

As a long term investor I’m not trying to predict when the next crash will occur and profit through a one-time macro event. I’m more interested in individual companies and whether they’d be able to survive and provide a long term benefit to my portfolio.

What are your thoughts on Home Capital Group Inc.?

Photo credit: 401(K) 2013 / Foter / CC BY-SA

Newsletter Sign-Up & Bonus

Have you enjoyed our content?

Then subscribe to our newsletter and you'll be emailed more great content from Dividend Growth Investing & Retirement (DGI&R).

BONUS: Subscribe today and you'll be emailed the most recent version of the Canadian Dividend All-Star List (CDASL).

The CDASL is an excel spreadsheet with an abundance of useful dividend screening information on Canadian companies that have increased their dividend for five or more years in a row.

The CDASL is one of the most popular resources that DGI&R offers so don't miss out!

I like the stock too. I am in awe of your analysis — much more thorough than mine when I bought HCG back in March or April.

Thanks. I started writing this one awhile ago and somehow it just kept getting longer and longer.

Thanks for the analysis. This was one on my list for further investigation. There is a good chance I will buy it after I research the rest.

Big slide on HCG today. 15%

Yeah, I ended up averaging down.

Bought some more today myself!

I do like your analysis & appreciate you sharing.

RBC blurb today detailed situation and pared back target price.

July 13, 2015

Home Capital Group Inc.

Downgrade to Underperform reflecting growth

concerns, not credit concerns

Our view: Downgrading to Underperform (was Sector Perform); lowering

12-month target to $39/share (was $48). Our downgrade does NOT reflect

credit concerns, but rather reduced earnings visibility and near-term

growth that appears to be even more challenged than our 2015 EPS

forecast (already low on the Street) suggested with potential implications

for 2016 growth.

Key points:

HCG pre-released Q2/15 non-prime residential originations of $1.29B

(below RBC at $1.66B), $280MM prime insured residential originations

(below RBC at $500MM) and $1.03 EPS (RBC at $1.04; consensus at

$1.06 with range of $1.04 to $1.09). HCG attributed origination weakness

to continued competition; conservative growth strategy; and terminating

certain broker relationships, but indicated it saw improving originations

late in Q2/15. HCG reports Q2/15 results on July 29.

We think this is an HCG-specific growth issue, NOT an early signal of

rising losses or broader housing stress; or origination growth issues for

other lenders. The pre-release underscores our concerns voiced earlier

this year about potential growth headwinds, particularly in the prime

insured market (prime originations missed our forecast in the past 4

quarters, non-prime missed in the last 2 quarters), hence why our EPS

forecasts were the low or below vs consensus.

We think reaching HCG’s target 3-5 average annual EPS growth of

8%-13% in 2015 is likely very difficult. To do so, we estimate H2/15

residential originations need to be ~150% higher than H1/15. Our EPS

forecasts go to $4.12 (was $4.24) in 2015 and $4.25 (was $4.79) in

2016, largely due to lower origination forecasts, but given lower expected

growth and profitability, we also reduced our expense growth forecasts.

Downgrading to Underperform (was Sector Perform); 12-month target

lowered to $39/share (was $48). HCG trades at 9.9x our 2016E EPS

forecast (EQB at 7.2x and FN at 7.6x).

Our Underperform rating reflects our view that HCG’s shares are fully

valued and likely to be range-bound reflecting reduced earnings visibility

as investors await further clarity on origination and EPS growth.

High-growth story historically; now potentially a steady growth story.

Long-term investors financially benefited from HCG’s successful growth

(since 2000, 25% EPS CAGR and >20% ROE), but that success is making

high growth more challenging, particularly given our view that industry

mortgage loan growth will slow in the next 2-3 years. We think HCG can

still deliver double digit EPS growth, but in the near-term, growth is likely

to be in the low to mid-single digits.

Thanks for posting this. I’ll be very curious to hear what the company has to say at the end of the month when they go over the Q2 results. I’m also curious if they’ll announce a dividend increase.

I thought the last sentence of the RBC analysis was interesting.

“We think HCG can still deliver double digit EPS growth, but in the near-term, growth is likely to be in the low to mid-single digits.”

I’m a long term investor so when I read something like this it looks like a buying opportunity to me. Time will tell though. There is a lot of speculation out there right now, so it is painful waiting for the July 30th Q2 conference call. The level of shorting in this company is very high too, which makes me a bit nervous. What do they know that I don’t?

Bought a little today. Will likely buy more as funds become available.

I bought today @ $36.21 and I’ve got an another open order @ $32.80 that might get triggered soon if the price keeps coming down.

Order got filled at $32 this morning.

Big price drop over the last couple of days .. are you buying more?

jonjon

I already averaged down @ $36.21 and again at $32. It’s currently around $32, so for now I’m happy with my current allocation. If it dropped another 10% I’d consider investing more.

I guess you are averaging down on cwb as well ?

I last bought TSE:CWB on Feb 23rd for $26.93 which was my 2nd purchase of the stock.

I’m not currently averaging down at these prices, but I have an open order for more at $24.

I averaged down on CWB myself recently.

Forgive the newbie question (I’m still learning), but how did you calculate the 10 year annual average return of 8.8% from that Google chart?

10 year average annual return = ((Total Return % + 1)^(1/10))-1.

So in this case the formula would be ((1.3308 + 1)^(1/10))-1 = 0.088 which is 8.8%.

Again, a good analysis. Thank you for sharing. HCG was not on my radar, but I’ll take a look at it. I don’t want to miss an opportunity to buy a good dividend growth company at a discount price of 29.87 per share.

Excellent analysis! Thank You

Thanks, glad you liked it.

Hey with recent short seller Marc Cohodes going after Home Capital what are you thoughts on his short thesis.

With Home Capital Group taking a bit of a hit at $29.10/share, are you interested in increasing your position. Would this be a good time to buy, some articles refer to HCG as a value trap. Any thoughts.

I bought @ $41, then averaged down at $36.21, $32, and then $28.35. Later I realized my exposure to financials was too high and that I started buying to early at $41, so I sold some HCG at $38.46 to lower my exposure to the company. You can read more about the sale and my reasons here: https://dividendgrowthinvestingandretirement.com/2016/04/portfolio-update-sold-part-home-capital-group-inc-position/

Hey, with recent carnage about HCG, I am interested to know your position now?

I’m expecting that there will be a dividend cut/elimination announced when the official earnings release happens. If that happens I plan to sell my shares.