Dividend Growth Investing & Retirement is supported by its readers through donations and affiliate links. If you purchase through a link on my site, I may earn a commission. Thanks! Learn more.

I have a hard time keeping my Dividend Stock Analyses under 3,000 words. A large portion of the analysis is spent explaining my valuation method and how I determine a target price. In an effort to make my analyses more concise, I’ve decided to create a separate post that describes my valuation technique and just link to the explanation from the dividend stock analysis. Hopefully this should make my dividend stock analyses easier to read, and if the reader wants a better understanding of my methods the information is still available in this post.

My Valuation Method

⭐ Find dividend growth stocks that have survived multiple recessions and increased dividends for 5, 10, 25+ years in a row.

There is a misconception out there that dividend investors only care about the dividend and don’t worry about the stock price. I can’t speak for everyone, but this certainly isn’t the case for me. I believe it’s important to purchase stocks at a reasonable to cheap price. This helps preserve your capital and will generally result in better returns. Rather than rely on just one method, I like to use a variety of different methods. Using this approach allows me better identify reasonable targets. I find that one measure could point to a cheap price, but another measure may not. For instance the P/E may point to a cheap price, but the P/Book may point to an expensive stock. By using a variety of different test you get a better idea if something is truly value priced.

I use the lowest price for the fiscal years to determine the 5 year, 10 year and 2008-2011 averages. Investors commonly use 5 and 10 year averages, but I like to include the fiscal 2008 to 2011 low price average, as I feel that the low prices during this era represent a reasonably low stock price. During 2008 and 2009 most companies experienced a really low price due to the Global Financial Crisis followed by increases in 2010 and 2011.

I use 6 main ratios to determine a fair price: Yield, Discount/Premium of the low price compared to the Graham Price, P/E, P/B, P/Sales and P/Cash flow. I like to look at both EPS and EPS from continuing operations so it ends up being a total of 8 ratios as the Graham Price an P/E both use EPS.

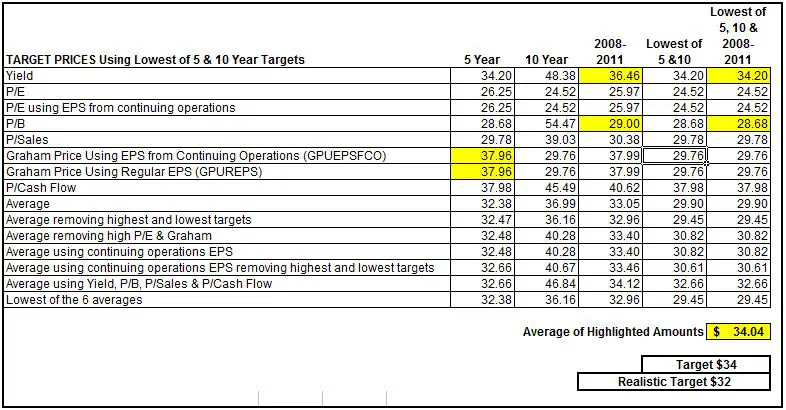

Once I’ve calculated the averages for these 8 different ratios I compare them to the most recent fiscal end in a table like the following.

* Calculation Notes: I compare the low price to the calculated Graham Price (GP) to determine the discount or premium to GP. I calculate the GP using the square root of (22.5 x Book Value x EPS). For EPS in this formula I use the lesser of the 3 year EPS average or the current EPS. If the GP calculated is negative then I set the Discount/Premium to GP as -25%. The other ratios are calculated in the normal fashion.

My valuation methods use historical averages, so it is important that you expect the company to continue to operate in a similar manner to its past. If you expect the company to change, these valuations become less useful.

Determining a Target Price

Now that I have these different averages, I can use them to determine a target price. Using these averages will create a lot of different target prices, so I like to compare this strategy to previous years. Ideally what I’m looking for is a strategy that would have given me a chance to buy the stock in two to three fiscal years in the past 10 fiscal years. It’s not always possible to test my strategy back 10 years, due to limited financial information, but I do my best.

I go through the information and highlight my conservative target prices in a table like below. The average of these is usually my target.

I would say that this strategy is quite conservative and as a result I don’t buy stocks very often. I’m usually waiting around for a few months before I’m able to buy something. This is fine by me as I’m young, so I’ve got the time and it pays to be patient. Sometimes my target price is too conservative, so much so, that occasionally I have to revise my target up. I like to use the yield as a way to gauge if my targets are realistic or not. For instance if my target price would result in a dividend yield that has never been paid by the company, then odds are the price isn’t going to come down that low. In these cases I adjust my target to a more realistic value. In rare instances I’ll adjust my target down further.

Before I buy a stock I like to look at Morningstar’s 5 star rating as a quick way of seeing what others think of the stock. I also like to compare my target price to Morningstar to see if my target price is in the same ballpark. If a stock has a 4 or 5 star rating then they consider the stock to be trading at discount to fair value. A 1 or 2 star rating indicates a premium to fair value and a 3 out of 5 rating suggests the price is close to fair value.

Bottom Line

This whole process is quite time consuming as it involves calculating target prices for each year of the past decade using 8 different ratios in order to find appropriately conservative targets. It is a rather complicated spreadsheet, but it’s a process that works for me and my investing style. I recognize that this procedure isn’t for everyone, so I’ve also written about how to come up target prices quickly.

What do you do to determine a target price?

Newsletter Sign-Up & Bonus

Have you enjoyed our content?

Then subscribe to our newsletter and you'll be emailed more great content from Dividend Growth Investing & Retirement (DGI&R).

BONUS: Subscribe today and you'll be emailed the most recent version of the Canadian Dividend All-Star List (CDASL).

The CDASL is an excel spreadsheet with an abundance of useful dividend screening information on Canadian companies that have increased their dividend for five or more years in a row.

The CDASL is one of the most popular resources that DGI&R offers so don't miss out!

![How to get free online access to the Value Line Investment Survey in Canada [+ list of Canadian stocks covered by Value Line]](https://dividendgrowthinvestingandretirement.com/wp-content/uploads/2018/08/Free-Online-Value-Line-Investment-Survey-Access-in-Canada-Map.-768x526.png)

Thanks a lot for all of the effort you put into your analyses. It is very much appreciated. There is one aspect of your methodology that is not clear to me – You only highlight a small number of cells in the table that you use to calculate your range of target prices. These highlighted cells are then averaged to come up with your target price.

How do you decide which cells to highlight?

Best Regards

What you see in that table is all the target prices calculated different ways for one year. I have a large excel file that calculates target prices in the same way, but for the past 10 years. The highlighted cells mean that this method of calculating the target price would have allowed you to buy the stock in 2 or 3 years of the past 10 years. I have a conservative investing philosophy, so I don’t want a target price that in the past would have given me an option to buy the stock every year as some years it would likely be overvalued. The same can be said for a target price that in past would never have given me an option to buy shares. This would be too conservative.

So basically the highlighted cells represent a 10 year back-testing of how that target price was calculated to see if you would’ve had the option to buy shares in the 2 or 3 years out of the past decade.

It can be difficult collecting all the data. I have target prices based on low price 10 year averages, which means to back test 10 years, I need about 20 years worth of financial information. It’s not always possible to get 20 years worth of the financial information that I want, so sometimes I have to estimate a bit, but I do my best.

Hope this helps clarify things.

I currently like the Graham method as described in The Intelligent Investor. There appears to be some faulty info on the web about his method, a formula, but it is really is first passing a set of criteria, then evaluating a stock for its intrinsic value. This is adjusted for inflation, bond prices, countries, but includes valuation of earnings, dividends, assets, liabilities and equity.